Article content

(Bloomberg) — The engines behind two years of European stock gains are losing power, leaving the region’s equities facing a void at a time when concerns over slowing growth and China tensions are testing investor confidence.

A luxury sector led by LVMH Moët Hennessy Louis Vuitton SE has tumbled over the past six months along with automotive firms, while in more recent months healthcare heavyweights such as Novo Nordisk A/S and tech leaders including ASML Holding NV have slid from their peaks. And with no obvious candidates to take the baton, the region’s equity performance has been left looking exposed.

Article content

Already this year, investors have withdrawn billions of dollars from Europe-focused funds and ETFs, in stark contrast to large amounts being pumped into US and international equity funds. A key issue is that the main drivers of the region’s gains have fallen off the pace of America’s Magnificent Seven group of tech companies.

“Leadership is changing” in the European market, said Ariane Hayate, a fund manager at Edmond de Rothschild Asset Management. “Smaller and more defensive sectors are leading the pack.”

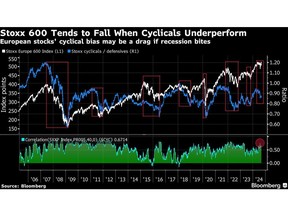

The European market is by definition a more cyclical one than its US counterpart, with those economically-sensitive sectors accounting for about two-thirds of the benchmark Stoxx 600. Consequently, the index’s correlation to the group is typically very high. But any support from these firms is now at risk with a double blow from slowing growth and trade risks with China.

“These companies also have a large percentage of their top line coming from the US and China,” said Barclays Plc strategist Ajay Rajadhyaksha. “If the risks of a global trade war rise, it is very easy to see these names de-rating somewhat out of trade concerns.”

Article content

Growth Problem

Meanwhile, Europe is geared more to Chinese demand, with firms getting about 8% of their revenues in the Asian country, according to Goldman Sachs Group Inc. strategists, compared with just 2% for S&P 500 peers.

While some say the risk of trade wars could be amplified in the event of a Donald Trump administration, Europe is already planning additional tariffs on Chinese-made electric vehicles in the face of heavy competition.

Another spillover effect from China’s economic problems is oil prices at lows unseen since 2021, blurring the outlook for Europe’s energy heavyweights such as BP Plc, Shell Plc and TotalEnergies SE. London’s mining stocks are also suffering from iron ore and copper prices falling.

By contrast, in the US, Big Tech has been a major driver, placing six stocks in the benchmark’s top 10, and making over 50% of returns.

In Europe, four of the 10 biggest contributors to the Stoxx 600 index’s returns this year are from the health care sector. When adding consumer staples firm Unilever Plc, the contribution from these five companies to its performance climbs to more than 30%. This defensive bias is unlikely to provide the same juice as cyclicals like luxury firms.

Article content

While earnings estimates have generally been holding up so far for 2025, Barclays’ Rajadhyaksha sees data surprises as more likely to hurt than help.

Profit estimates may indeed be at risk for the region. A Citigroup Inc. gauge of earnings revisions that account for profit upgrades and downgrades has been negative for most of the summer.

Sector Rotation

With the European market’s former darlings fading, investors are heavily rotating as they look for new opportunities. For Gilles Guibout, a Paris-based portfolio manager at Axa Investment Managers, some segments of the stock market look promising should the economy settle for a soft landing.

“Rising dividends could help raise valuations and who pays dividends? Banks and utilities,” he said.

European banks have had a stellar year so far, rising 18%, and he argues there is room for further gains given low valuations. Investor interest for the sector has also grown since UniCredit SpA Chief Executive Officer Andrea Orcel said he was considering a full takeover of Germany’s Commerzbank AG.

“For utilities, lower interest rates provide immediate relief and they already have started to outperform this summer. There are prospects of rising dividends, rising earnings and multiple expansion in this space,” Guibout added.

Moving forward, other fund managers believe there are segments of the stock market ready to take over market leadership, if a recession is averted.

“If we’re indeed entering a soft landing, then it makes sense to bet on the broadening of the rally, to bet on the laggards, such as small and mid-caps,” said Amelie Derambure, a senior multi-asset portfolio manager at Amundi in Paris. “That’s why we’re keeping a very close eye on growth momentum indicators. Laggards could be the market’s next driver if economic growth bounces back.”

Share this article in your social network