A barrage of euro-zone economic data this week will deliver crucial information for the European Central Bank as officials look for signals on whether to resume interest-rate cuts in September.

Author of the article:

Bloomberg News

Alexander Weber

Published Jul 29, 2024 • 4 minute read

You can save this article by registering for free here. Or sign-in if you have an account.

wnq3o1p[9cq(e5o5093}kghp_media_dl_1.pngEurostat, Bloomberg survey of ec

Article content

(Bloomberg) — A barrage of euro-zone economic data this week will deliver crucial information for the European Central Bank as officials look for signals on whether to resume interest-rate cuts in September.

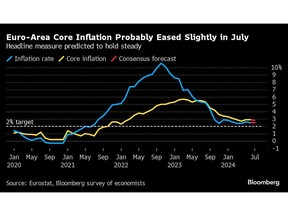

A report on Wednesday will probably show inflation at 2.5% for a second month, according to the median forecast of 36 economists in a Bloomberg survey. A Nowcast by Bloomberg Economics is more optimistic, showing a slowdown to 2.3%.

Advertisement 2

This advertisement has not loaded yet, but your article continues below.

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, Victoria Wells and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account.

Share your thoughts and join the conversation in the comments.

Enjoy additional articles per month.

Get email updates from your favourite authors.

Sign In or Create an Account

or

Article content

Some relief may come from the core measure of inflation that excludes volatile items such as energy and food. Analysts predict it edged down to 2.8%.

Since the ECB left borrowing costs on hold this month, officials have stressed that the next decision in September hinges on the string of economic data due to arrive by then. Investors expect there to be a cut, pricing an almost 90% probability of a move.

This week will also see the release of figures on second-quarter economic growth, which may show that the recovery from months of stagnation is proving less dynamic than initially expected.

Output probably increased 0.2% in the 20-nation bloc, down from 0.3% in the first three months of the year, according to the poll and the BE Nowcast. Momentum in Germany, Italy and Spain are predicted to have slowed.

Read more: Scholz Is Failing to Engineer a Liftoff for the German Economy

ECB President Christine Lagarde highlighted the importance of such information when she declared this month that the next decision — for which her staff will also produce a new set of economic projections — is “wide open.”

Top Stories

Get the latest headlines, breaking news and columns.

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Top Stories will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

Advertisement 3

This advertisement has not loaded yet, but your article continues below.

Article content

“It’s clear that between now and September, we will be receiving a lot of information,” she said. “I’m afraid that it’s going to be a bit of a busy summer.”

Others have doubled down on that sentiment since then. Vice President Luis de Guindos said that “data-wise, September is a much more convenient month for taking decisions” while Slovakia’s Peter Kazimir suggested to wait for the “much-anticipated September ‘health check.’”

Not a single Governing Council member is scheduled to speak this week, which will allow markets to draw their own conclusions on the numbers.

What Bloomberg Economics Says…

“Our base case is data released between now and the ECB’s September policy meeting will pave the way for another rate cut then. Favorable energy base effects should leave headline CPI within touching distance from the ECB’s 2% target in the August print and there will likely be more evidence underlying price pressure is easing, both in services inflation and in the wage data.”

-Ana Andrade, economist. Read the full week-ahead here

A first bout of numbers already arrived last week, painting a surprisingly negative picture of the euro-zone economy. Private-sector output probably failed to grow in July, according to business surveys by S&P Global, while Ifo’s monthly survey pointed to a darkening mood among German companies.

Advertisement 4

This advertisement has not loaded yet, but your article continues below.

Article content

The emerging picture of fizzling recovery and stubborn price pressure may prove challenging for ECB officials to navigate. But details matter more than usual, putting extra weight on the final inflation readings arriving in the middle of July and August.

For now, services inflation remains a key measure as labor costs play an important role in that sector. ECB Executive Board member Isabel Schnabel said the persistence of that gauge was a central reason why the last mile is still proving difficult.

“A repeated surprise in services inflation is at least a reason for taking a closer look,” she told Frankfurter Allgemeine Zeitung in an interview published late last week.

The services number remained stuck at 4.1% in June, more than twice the overall target — making it a focal point in the runup to the September decision, according to ING economist Carsten Brzeski.

“If I had to single out a few key data, I think the profile of the staff September inflation forecasts as well as actual services inflation data over the next two months will be the most important data to tilt the balance to either side,” he said.

Advertisement 5

This advertisement has not loaded yet, but your article continues below.

Article content

The central bank currently projects that inflation will reach its goal in the final quarter of 2025. It’s important that the update after the summer still shows inflation at that time at 2% or lower, according to Brzeski.

T. Rowe Price economist Tomasz Wieladek agrees that price pressures in the services sector may end up playing a decisive role.

“If they get two more well behaved readings, this would be a strong signal of disinflation and will support a cut in September,” he said. If growth data also remain weak, there could even be a discussion “about a faster pace of cuts or a larger cut in September,” he said.

Wages remain a central issue, as a slowdown to more sustainable levels is seen as a precondition for inflation to return to target. Recent developments will become more clear when the ECB publishes its indicator on negotiated pay and with a Eurostat release on compensation per employee.

But officials will probably look at more forward-looking indicators like the central bank’s own wage trackers to be certain that the anticipated decrease will materialize.

“We will need to see a lot of evidence across multiple indicators for the ECB to significantly change the wage forecast in 2025,” according to Wieladek. “Wage information will matter a little bit less over the summer.”

—With assistance from Barbara Sladkowska and James Hirai.