Traders are betting against Canada’s biggest banks as the risk of mortgages and other loans going bad rises with the economy still struggling.

Author of the article:

Published Jul 25, 2024 • 3 minute read

Article content

(Bloomberg) — Traders are betting against Canada’s biggest banks as the risk of mortgages and other loans going bad rises with the economy still struggling.

The issues aren’t new. For the last 12 months, Canadian lenders have come under pressure as high interest rates and inflation weighed on credit growth. Banks also were forced to set aside more money for potentially sour loans, which cut into profits. And now they’re dealing with strained Canadian consumers who are facing a wave of mortgage renewals.

Advertisement 2

Article content

Under Canada’s home loan system, borrowers can’t get 30-year fixed-rate mortgages the way they do in the US. Rather, Canadian mortgages typically have terms of five years with different amortization lengths, meaning homeowners need to refinance multiple times over the course of paying off the loan. With interest rates having soared since 2019, despite the Bank of Canada’s recent rate cuts, borrowers who need to re-up their loans in the near future are facing “payment shock,” according to the risk outlook the Office of the Superintendent of Financial Institutions released in May.

“The key vulnerability here is the cohort of borrowers that took out a mortgage between 2020 and 2022,” Hedgeye analyst Drago Malesevic said during an investor call last week.

As a result, short interest ratios on Canadian bank stocks are rising. Laurentian Bank’s short interest as a percentage of its float is now 4.7%, up from 3.4% at the start of April. And Canadian Imperial Bank of Commerce’s is 3.8%, up from 3.3% at the beginning of the second quarter.

Winning Bets

Betting against Canadian banks has been a winner this year, with shorts up $243 million in 2024 on wagers against the country’s “Big Six” banks: Toronto-Dominion Bank, Royal Bank of Canada, Bank of Montreal, Bank of Nova Scotia, CIBC and National Bank of Canada. But a recent rally in Canadian stocks has traders beginning to cover those positions, as short sellers have seen two-thirds of their paper gains in short bank wagers disappear in this month alone, data from S3 Partners show.

Top Stories

Article content

Advertisement 3

Article content

To be sure, big bets against these stock aren’t new. In 2017, famed “Big Short” investor Steve Eisman of Neuberger Berman Group said he was short the Canadian banks. Last year, during the regional banking crisis, TD became the world’s most-shorted bank stock.

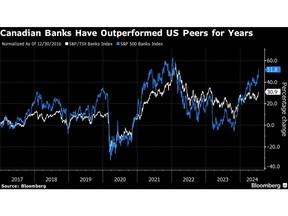

However, the trade historically has been a money-loser, earning the nickname The Great White Short on Toronto’s Bay Street. During the Global Financial Crisis, the S&P/TSX Banks Index fell 34% in 2008 before rebounding 54% in 2009. By contrast, the S&P 500 Banks Index fell 50% in 2008 and another 9% in 2009. Since 2017, when Eisman said he was short Canada’s banks, the group has climbed 52% compared with a 31% jump for the US banks group. Eisman declined a request for comment.

“Canadian banks and Canadian housing, betting against those two things has been like a pretty heavy widow maker over the past decade,” Malesevic said in an interview.

Earnings Challenges

In the last year, however, it’s been a money-maker. And going forward, the Big Six banks will see their earnings challenged by rising credit losses, an economic slowdown, declines in consumer spending and rising delinquencies, according to Hedgeye’s Malesevic and Josh Steiner. CIBC and Bank of Nova Scotia are the top two short ideas in the sector for the firm, which provides investment advice to hedge funds.

Advertisement 4

Article content

On the flip side, an uptick in fee-based revenues from capital markets and other business lines could buoy earnings this year, said Paul Harris, partner at Harris Douglas Asset Management in Toronto. He also expects the group to set aside enough capital to cover its credit losses.

Still, the sector is largely dependent on the rate-cut narrative as the economy slows down. If the central bank hadn’t cut interest rates, “that was when we were going to press the panic button because at that point we felt that was the tipping point as to being too late to cut rates to be able to minimize the damage to the economy,” said John Aiken, senior analyst and director of research for Canada at Jefferies Financial Group Inc.

Rate cuts will drive a lot of Canadian bank performance over the next few quarters, Aiken said in an interview, adding that potential for additional cuts reduces concerns about the impact of mortgage renewals. The move may also help to propel lending growth from the anemic levels in the market right now, he said.

“Shorting Canadian banks has been a terrible trade over the years,” Harris said. “And I think it will continue to be a terrible trade.”

(Adds detail to John Aiken’s role at Jefferies in third to last paragraph.)

Article content