Companies will have to impress as expectations are elevated, especially for megacap technology stocks

Author of the article:

Published Jul 15, 2024 • Last updated 13 minutes ago • 4 minute read

Article content

A non-stop rally in U.S. stocks since April is facing a major test as companies start reporting earnings this week.

The S&P 500 index has notched one record after another, powered by the so-called Magnificent Seven and all things artificial intelligence. Companies will have to impress as expectations are elevated, especially for the megacap technology stocks. Though still robust, big-tech earnings are projected to slow.

Advertisement 2

Article content

Analysts estimate that second-quarter profits will rise 9.3 per cent for members of the benchmark over the prior-year period, which will be the biggest such expansion since the last three months of 2021, data compiled by Bloomberg Intelligence show.

The S&P 500 rose 3.9 per cent in the last quarter, and has since advanced another 2.8 per cent through Friday’s close.

Article content

“The hurdle is high,” Ed Clissold, chief U.S. strategist at Ned Davis Research Inc., said in a note to clients. “Even strong beats may not be enough for the Magnificent Seven growth rate to continue to accelerate.”

Investors will look for clues on the health of the consumer, especially after PepsiCo Inc.’s sales disappointed last week and Delta Air Lines Inc. said domestic carriers were struggling to fill planes even in the all-important summer travel season.

Earnings season kicked off on Friday, with banking bigwigs JPMorgan Chase & Co., Wells Fargo & Co. and Citigroup Inc. reporting generally mixed results. Other companies including BlackRock Inc. — the world’s largest asset manager — Netflix Inc. and JB Hunt Transport Services Inc. will deliver results next week.

Investor

Article content

Advertisement 3

Article content

Here’s a look at five key themes to watch.

Broader rally

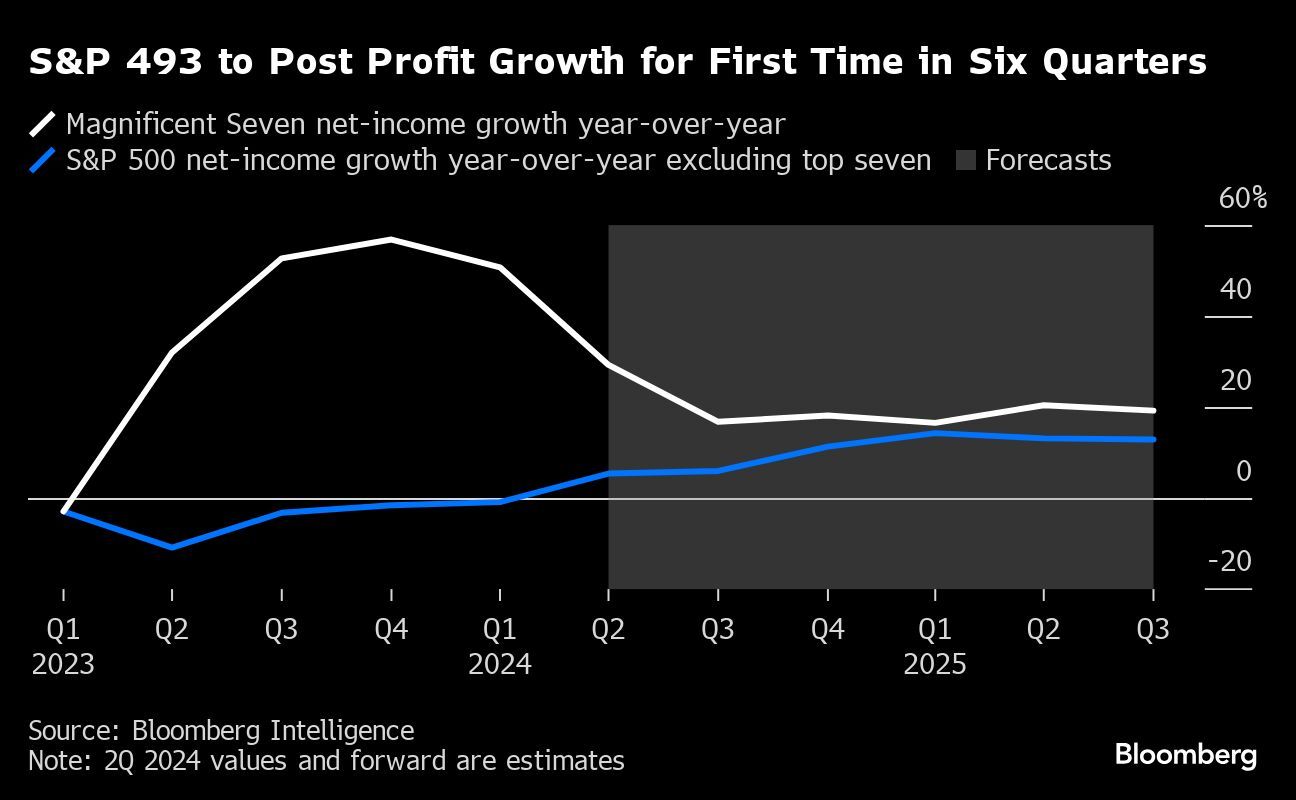

For the first time since 2022, investors will likely shift their attention to the rest of the 493 companies in the S&P 500. Companies outside of tech are expected to report their first quarterly earnings growth in at least six quarters. Profits are estimated to grow 5.4 per cent and are seen accelerating toward double-digit increases by the final three months of the year, according to data compiled by BI.

“Growth is broadening out and so should the market,” Bank of America Corp.’s equity and quant strategists Ohsung Kwon and Savita Subramanian said in a note this week.

The Magnificent Seven — Apple Inc., Microsoft Corp., Alphabet Inc., Amazon.com Inc., Nvidia Corp., Meta Platforms Inc. and Tesla Inc. — is on course for a slowdown in growth. Profits are expected to rise by 29 per cent, compared to average earnings growth of 35 per cent in 2023, when the rest of the S&P 500 fell five per cent, according to BI.

Mixed industry outlooks

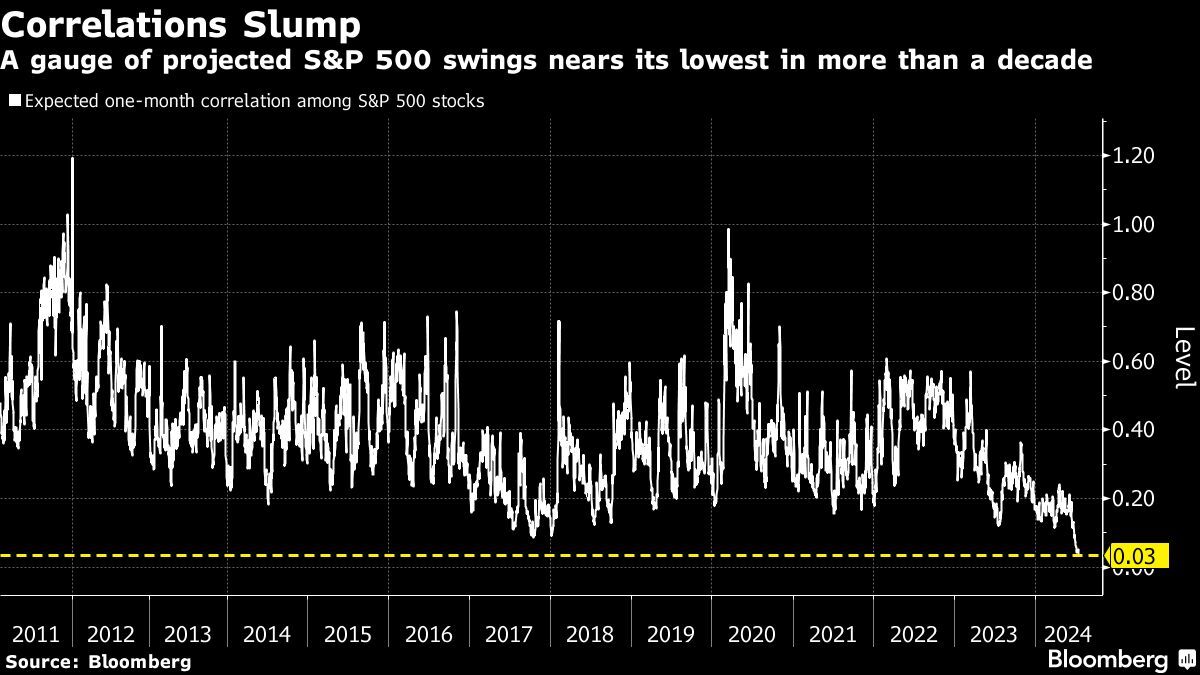

Traders are betting that share prices will not move in unison this earnings season, making it difficult to pick winners. While inflation is ebbing, differing outlooks for S&P 500 industries have left a gauge of the expected one-month correlation in the index’s stocks hovering at its lowest in more than a decade, data compiled by Bloomberg show. A reading of one means securities will move in lockstep; it’s currently at 0.03.

Advertisement 4

Article content

This comes as three of the 11 groups — tech, communication services and health care — are set to post profit expansions of more than 10 per cent, while profits at real estate, industrials and materials companies will likely shrink. Low correlations are welcomed by fund managers looking to beat indexes through stock picking.

At the same time, options are implying an average move of 4.3 per cent in either direction on earnings for S&P 500 members, which is above the historical average of 4.1 per cent since 2012, Vishal Vivek, equity trading strategist at Citigroup, said.

“Investors chasing alpha should focus on earnings-related moves,” he said, especially as earnings-day volatility relative to non-earnings days has increased to its highest level since 2018.

China recovery

A long-awaited earnings recovery in China has so far failed to come to fruition and results aren’t expected to improve much in the second half of 2024. Hurting growth prospects are a slew of deep-rooted issues — from a housing sector downturn to demographic headwinds — that are hard to resolve.

Advertisement 5

Article content

Home appliance and new electric-vehicle makers are among those well-placed to benefit from the country’s export boom. Still, the earnings trajectories of these industries face the risk of derailing as Western governments set up trade barriers. The economic impact of such tariffs or restrictions has been limited so far, but may eventually erode profits at corporations.

U.S. companies and investors watch for signs of any weakness in China’s economy that can ripple through the global economy, namely consumer discretionary, technology, industrials and autos.

AI trade

Artificial intelligence will continue to be in the spotlight. As the megacaps’ pace of earnings expansion is set to decelerate, close focus will be on how companies such as utilities and data centres are deploying capital into AI and whether those investments will boost stock valuations.

“The AI trade is under increasing scrutiny,” Goldman Sachs Group Inc. strategists Ryan Hammond and David Kostin said in a note. “Investors are increasingly concerned about the potential returns to the hyperscalers’ AI investment spending,” they said, referring to Amazon.com, Meta, Microsoft and Alphabet.

Advertisement 6

Article content

Analyst sales estimates for the companies have not increased commensurate with investment spending, they added.

The strategists recommend looking at “sales revisions as a key indicator for the durability of the AI trade.”

Election-year risks

The one wild card for equities this year is the U.S. presidential election and the policy-related uncertainties that come with it. Companies that make electric vehicles, EV batteries, semiconductors, solar cells, critical minerals, steel and aluminum face risks, and regulation-heavy groups such as financials and health care will be in the crosshairs. Investors will be parsing earnings calls for comments and outlooks that will hint at potential risks to companies’ bottom lines.

Article content