European Central Bank officials may be about to prime investors for another interest-rate cut, though only after one of the Governing Council’s longest-ever summer breaks between decisions.

Author of the article:

Bloomberg News

Craig Stirling and Marilen Martin

Published Jul 13, 2024 • 7 minute read

You can save this article by registering for free here. Or sign-in if you have an account.

vyqusvimjn8vshrkb4es47gw_media_dl_1.pngOffice for National Statistics

Article content

(Bloomberg) — European Central Bank officials may be about to prime investors for another interest-rate cut, though only after one of the Governing Council’s longest-ever summer breaks between decisions.

With a move on Thursday effectively ruled out as policymakers take time to assess the strength of lingering inflation pressures, traders are likely to watch closely for any clues offered by President Christine Lagarde on prospects for the Sept. 12 decision.

Advertisement 2

This advertisement has not loaded yet, but your article continues below.

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, Victoria Wells and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, Victoria Wells and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account.

Share your thoughts and join the conversation in the comments.

Enjoy additional articles per month.

Get email updates from your favourite authors.

Sign In or Create an Account

or

Article content

By then, the ECB will have seen two more monthly consumer-price readings, and have newly-compiled forecasts in hand as well. Several policymakers have stated a preference for acting at such quarterly occasions when fresh projections are available.

Officials may also have a clearer view by then of the Federal Reserve’s intentions. With fresh data showing US inflation broadly cooled to the slowest pace since 2021, speculation is mounting that policymakers in the US will also seek to cut rates in September.

New information that the Governing Council will see before its decision on Thursday includes a reading of industrial production in May on Monday, which is forecast to show a second month of contraction, and a final measure of inflation for June on Wednesday.

Aside from questions on the path of borrowing costs, the ECB president may also be quizzed this week on France, which faces heightened scrutiny in financial markets amid concerns about its fiscal outlook after snap elections produced a hung parliament. That situation may also focus European finance ministers set to meet in Brussels on Monday.

Advertisement 3

This advertisement has not loaded yet, but your article continues below.

Article content

What Bloomberg Economics Says:

“The ECB’s July 18 meeting will be closely watched by investors to fine-tune their expectations for the timing of the next rate reduction, even though it’s almost certain to leave rates unchanged this month. Lagarde is likely to hint at another move in September, without being too committal.”

—David Powell, senior euro-area economist. For full analysis, click here

Lagarde’s press conference could resonate more than usual, as colleagues heading to the beach during the summer fall largely silent at this time. Similarly, any appearance by an ECB official at the Fed’s annual retreat in Jackson Hole, Wyoming, in late August, could draw extra attention.

This year’s eight-week gap between rate decisions is the longest summer pause for the Governing Council since the height of the pandemic in 2020. The ECB held monthly meetings for much of its history, before it introduced bigger breaks between gatherings starting in 2015.

Elsewhere, reports that may show slowing Chinese growth, declining US retail sales and decelerating inflation in the UK and Canada, along with rate decisions in Indonesia, Egypt and South Africa, are among the highlights. Investors will also scour new global economic forecasts from the International Monetary Fund scheduled for Tuesday.

Top Stories

Get the latest headlines, breaking news and columns.

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Top Stories will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

Advertisement 4

This advertisement has not loaded yet, but your article continues below.

Article content

Click here for what happened in the past week and below is our wrap of what’s coming up in the global economy.

US and Canada

On Monday, Federal Reserve Chair Jerome Powell will sit for an interview at the Economic Club of Washington in the wake of data showing a welcome softening in inflation. Investors will watch for clues on whether US central bankers are confident enough of a sustained slowdown in price pressure to cut interest rates.

Powell’s event opens a week of appearances by other high-profile Fed officials, including Fed Board members Adriana Kugler and Christopher Waller, and New York Fed President John Williams.

Retail sales are the highlight of the US economic data calendar. Economists project a decline in the June value of sales, partly due to a cyberattack that disrupted auto dealers and a drop in gas station receipts.

So-called control group sales, which exclude autos, gasoline, food services and building materials, are expected to downshift. The measure, used to calculate gross domestic product, is seen illustrating to extent to which budget-conscious consumers are limiting discretionary purchases.

Advertisement 5

This advertisement has not loaded yet, but your article continues below.

Article content

A day after Tuesday’s retail figures, the government is forecast to report a modest gain in June new home construction from the slowest pace in four years. Builders have benefited from lean inventories in the resale market even as demand remains restrained by high borrowing costs.

Also Wednesday, the Fed will release its June industrial production report, as well as its Beige Book anecdotal report of economic conditions in each of the central bank’s 12 districts.

In Canada, meanwhile, the inflation print for June will be crucial to guiding the Bank of Canada’s rate decision due on July 24, particularly after that measure unexpectedly quickened in May. The central bank will also publish its consumer and business surveys for the second quarter, and we’ll get retail sales data for May and a flash estimate for June.

For more, read Bloomberg Economics’ full Week Ahead for the US

Asia

The health of China’s economy will top the agenda in Asia as analysts, investors and policymakers scrutinize the latest quarterly growth figures and a slew of monthly readings.

The world’s second-largest economy is expected to have expanded at a slower pace of 5.1% in the June quarter versus a year earlier, while still staying on track to achieve Beijing’s growth target for 2024.

Advertisement 6

This advertisement has not loaded yet, but your article continues below.

Article content

Monthly factory output will show a second-straight slowing from robust levels, while retail sales are also set to soften, according to forecasts.

Despite hopes among investors that China will consider more stimulus to goose its economy, none of the figures are likely to point to an urgent need to do that.

The release of that data coincides with a four-day gathering of China’s top leadership — a twice-a-decade event — that may focus on initiatives to revitalize growth.

Elsewhere in the region, Indonesia’s central bank is predicted to keep rates on hold on Wednesday, with New Zealand unveiling its latest inflation numbers and Singapore releasing export figures the same day.

Malaysia, Japan and India also have trade data due during the week. Kuala Lumpur will issue its GDP numbers at the end of the week.

Australian employment growth on Thursday is expected to show a halving in the number of new jobs created.

Nationwide price growth in Japan is seen strengthening to 2.7% in June data out Friday, an outcome that might fuel expectations the Bank of Japan will consider combining a cut in bond purchases with a rate hike at its meeting later this month.

Advertisement 7

This advertisement has not loaded yet, but your article continues below.

Article content

For more, read Bloomberg Economics’ full Week Ahead for Asia

Europe, Middle East, Africa

Among data releases, the UK will draw most attention in the region.

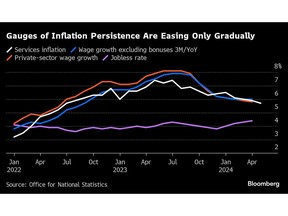

The latest reading of consumer prices on Wednesday may show services inflation slowed for a fifth month in June, to 5.6% – still well above the 2% goal targeted by policymakers. The country’s latest wage numbers will be released on Thursday, with regular pay growth predicted to cool below 6% for the first time in 20 months, in figures covering the quarter through May.

Meanwhile, retail sales for June, due on Friday, probably fell, while other data the same day will mark the first reading on the public finances that Chancellor of the Exchequer Rachel Reeves has seen since taking office.

The week’s figures are the last major releases before the Bank of England’s Aug. 1 decision, when officials will judge whether to cut rates for the first time since the start of the pandemic.

For more, read Bloomberg Economics’ full Week Ahead for EMEA

Turning to the African continent, data from Nigeria on Monday will likely show the inflation rate in June held near 34%, helped by a more stable naira. Analysts expect that it could begin to slow, starting this month, partly due to a high base effect.

Advertisement 8

This advertisement has not loaded yet, but your article continues below.

Article content

Three central bank rate decisions are scheduled:

Egypt is expected to hold its rate at 27.25% on Thursday, even with inflation slowing to a 17-month low. The central bank is likely to keep monetary policy tight for at least several more months in a bid to further tame the country’s cost-of-living crisis.

In South Africa the same day, policymakers are also forecast to leave their rate unchanged for a seventh straight meeting to rein in inflation most recently at 5.2%. Governor Lesetja Kganyago has repeatedly said that officials won’t cut rates until inflation is firmly at 4.5%, where the central bank prefers to peg expectations.

In Angola on Friday, policymakers are set to raise their key rate, currently at 19.5%, for a third straight meeting, given persistent inflation and currency pressures.

Latin America

Four of Latin America’s major economies will report activity readings for May, key proxies for GDP that central bankers will monitor closely amid ongoing concerns about growth and inflation.

Brazil and Peru, where policymakers have recently put easing cycles on pause, will report their data on Monday. Over recent weeks, Brazil President Luiz Inacio Lula da Silva has renewed his criticism of high borrowing costs that he sees as a threat to the region’s largest economy, while Peru’s fastest growth in more than two years contributed to central bankers’ decision to hold rates steady for a second straight time.

Advertisement 9

This advertisement has not loaded yet, but your article continues below.

Article content

In Colombia, which will report its data on Thursday, first quarter growth that came in below forecast led President Gustavo Petro to call for faster rate cuts, a push policymakers defied in late June.

Argentina will follow on Thursday afternoon. South America’s second-largest economy entered recession at the start of this year, shrinking 2.6% from the final three months of 2023 as President Javier Milei’s brutal spending cuts weighed on consumption and activity.

For more, read Bloomberg Economics’ full Week Ahead for Latin America

—With assistance from Vince Golle, Paul Jackson, Andrew Langley, Matthew Malinowski, Tom Rees, Monique Vanek and Paul Wallace.