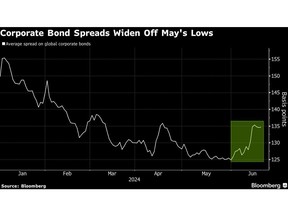

Global corporate bond spreads are on track to turn in their first month of weakening since late last year, reigniting the debate about the relative value of credit versus other fixed-income classes heading into the second half of 2024.

Author of the article:

Bloomberg News

Finbarr Flynn and Tasos Vossos

Published Jun 22, 2024 • 6 minute read

You can save this article by registering for free here. Or sign-in if you have an account.

e7aidn7fo418hb[w[dd2lbx1_media_dl_1.pngBloomberg

Article content

(Bloomberg) — Global corporate bond spreads are on track to turn in their first month of weakening since late last year, reigniting the debate about the relative value of credit versus other fixed-income classes heading into the second half of 2024.

Spreads on corporate bonds including junk and investment-grade notes have widened by about 10 basis points so far in June, from around the lowest levels seen in three years, a Bloomberg index shows. Meanwhile, yield premiums on those notes as well as US high-grade bonds are rising from levels touched in May which have only been seen for less than 1% of the period since the 2008 global financial crisis, the data shows.

Advertisement 2

This advertisement has not loaded yet, but your article continues below.

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, Victoria Wells and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, Victoria Wells and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account.

Share your thoughts and join the conversation in the comments.

Enjoy additional articles per month.

Get email updates from your favourite authors.

Sign In or Create an Account

or

Article content

While heavy spread widening would make credit less attractive compared with Treasuries, Goldman Sachs Group Inc. strategists led by Lotfi Karoui don’t see that happening. The bank forecasts US high-grade spreads ending 2024 at 90 basis points and junk spreads at 291, compared with current Bloomberg index levels of 94 basis points and 314 basis points, respectively.

“We’re in this holding pattern of the macroeconomic backdrop, which is not too hot, not too cold,” said Neeraj Seth, chief investment officer and head of Asia-Pacific fundamental fixed income at BlackRock Inc. in Singapore. That’s normally a “good environment” for credit, and while spreads may widen at different junctures, there’s still potential for them to tighten back over a six-to nine-month outlook, he said.

Investors aren’t getting paid a lot for credit risk, according to abrdn investment director Luke Hickmore. However, he still sees an argument for holding corporate debt as spreads could remain around current levels for several more years, similar to the period between 2004 and 2006 when interest rates stayed high.

Top Stories

Get the latest headlines, breaking news and columns.

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Top Stories will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

Advertisement 3

This advertisement has not loaded yet, but your article continues below.

Article content

“Fundamentals are pretty good at the moment” after many companies cut debt, he pointed out. “With de-leveraging, a fairly stable economic outlook and the high interest-rate profile, you may as well get the extra carry.”

A decline in US Treasury yields this month on renewed bets that the Federal Reserve will cut interest rates at least once this year is partly responsible for credit spreads widening, as corporate bonds usually take time to catch up to moves in more liquid government debt.

“Historically spreads struggle to tighten when yields are declining, until they stabilize again,” JPMorgan Chase & Co. strategists Eric Beinstein and Nathaniel Rosenbaum wrote in a note this month. It’s uncertain whether it will cause some investors to step back, as was observed earlier in the month, they added.

For some, the problem with corporate credit has more to do with its meager yield pick-up relative to its risks than with any clear signs of weakness in economies or problems on corporate balance sheets.

Noah Wise, a portfolio manager at Allspring Global Investments, says he’s been taking advantage of the recent rally in high-yield bonds to lower his exposure to the debt. He added that he prefers US agency mortgages that have AA type ratings with spreads in the 50s.

Advertisement 4

This advertisement has not loaded yet, but your article continues below.

Article content

“There is a historically narrow amount of incremental spread for credit risk at this point, so valuations aren’t attractive,” he pointed out. “We’re relatively lightly positioned.”

So far this year, corporate bonds have outperformed Treasuries. That’s expected to continue, with Goldman strategists seeing both high-grade and high-yield bonds in dollars and euros outperforming government bonds this year.

European junk bonds may deliver 5% in excess returns in 2024, while their US equivalents may generate 3.7%, the bank said in a June report, while European and US high-grade securities may deliver 2.7% and 1.6% respectively on the same measure.

Metrics at US high-yield debt issuers have been mixed. Firms showed broad-based deterioration in the first quarter with profit margins dropping to a three-year low, though leverage was comfortably below the long-term average, JPMorgan strategists including Nelson Jantzen wrote in a June 12 note.

Click here to listen to Arini’s Lemssouguer talk about how junk companies are hitting a wall.

“In this type of environment where spreads are very tight, the front end of the curve, shorter-dated bonds, is where I’ll be looking for carry,” said Marvin Kwong, a fixed-income portfolio manager at M&G Investments who likes Asian bank capital securities. “In the long end of the curve, given where spreads are, I would rather opportunistically position in Treasuries or futures given the volatility” to take advantage of any move lower in yields, he added.

Advertisement 5

This advertisement has not loaded yet, but your article continues below.

Article content

Kwong expects the Fed to cut one or two times this year and three to four times next year, with economies broadly holding up.

Gabriele Foa, a portfolio manager at Algebris Investments, warns that “the fundamental picture is deteriorating a little bit and credit spreads are at absolute tights.” “This is already an alarm bell,” he said. “We have a few longs but overall we have the most cautious positioning we’ve had in credit in the past couple of years.”

For Pauline Chrystal, a fund manager at Kapstream Capital in Sydney, the tight valuations on US dollar-denominated corporate bonds are also a concern. She prefers Australian credits where valuations are less stretched.

“That credit spreads could tighten another 20 or 30 basis points is something that I just find really hard to believe,” she said. “But if momentum is very strong and every one of your peers is continuously investing in credit, you can’t just sit in cash.”

Week in Review

Some money managers that buy junk bonds have been pouring money into investment-grade notes instead, because the yields can be almost as high now.

Private equity investors are clamoring for their payouts. A risky approach to meeting their demands — namely dividend recapitalizations — is setting records and getting more popular.

Bank of America Corp.’s Dan Mead expects US blue-chip bond market activity to slow down through the end of this year, after borrowers gorged on debt in the first half, enticed by attractive yields now and avoiding election volatility later.

The US Supreme Court upheld a 2017 tax on American-owned businesses’ foreign profits, rejecting an appeal that could have saved companies hundreds of billions of dollars.

President Emmanuel Macron’s surprise election call has highlighted France’s prominence in European credit markets.

Chinese companies are joining this year’s biggest run of Japanese-currency note issuance by the nation’s borrowers since 1986 in a still-small but growing market.

Investors in the $1.3 trillion collateralized loan obligation market are expecting to benefit from Norinchukin Bank’s pains, as the Japanese whale looks to dispose of some sovereign bonds and rotate its investments into other markets.

Enel Finance International tapped the US investment-grade bond market for the first time after missing emissions targets and boosting bond coupons.

Canadian energy pipeline company Wolf Midstream is preparing to sell C$600 million ($438 million) of junk bonds.

Home Depot Inc. sold $10 billion worth of bonds in the US investment-grade market to help finance its acquisition of building-products distributor SRS Distribution Inc.

Hertz Global Holdings Inc. increased the size of a junk-bond sale by a third to $1 billion, as the car-rental company works to bolster its balance sheet after a misstep on its electric vehicle fleet.

After a two-year absence from the asset-backed securities market, Carlyle Aviation Partners is returning with a bond sale backed by commercial aircraft, a market where issuance could keep climbing as new plane sales come under pressure.

CLO managers, the biggest investors in leveraged loans, have long taken a backseat role when borrowers get into trouble. That’s starting to change.

On the Move

Christopher Horn, a widely recognized industry leader in the regulation of securitization transactions, has joined Cadwalader, Wickersham & Taft as a partner in the firm’s New York office.

San Francisco-based Community Investment Management has hired Ravi Vukkadala as country head for its India operation, just weeks ahead of the nation’s entry into a key global bond index.