As Melbourne Water redesignates flood zones, home owners in Kensington Banks could be faced with futures where their homes are valued at less than what remains on their mortgage.

An industry expert says thousands of homes across Australia could be “uninsurable” in coming years.

Residents of the Kensington Banks development, located about five kilometres from Melbourne’s CBD, were recently told by the local water authority they now live in a flood zone and it is estimated by realtors they could see property price dips of 20 per cent.

Roger Hadgraft says the news came as a shock to him, after new flood modelling was done for the first time in two decades.

“It’s crazy, because we believed that this area was immune from a 100-year flood,” Mr Hadgraft, a Kensington Banks resident, told 7.30.

Mr Hadgraft had checked the available flood maps before purchasing his property, but those maps are now obsolete. He says it has left him concerned about the value of his property.

“You do worry about the future value of the house because you think … you can easily lose a quarter or a third of the value,” he said.

Another resident who 7.30 spoke to but wished to remain anonymous was angry at Melbourne Water.

“We’ve got a big mortgage, what’s going to happen if we need to sell and all of a sudden the property is worth less than we’ve got to pay back?

“How is it acceptable that we’ve got flood mapping … that’s 20 years out of date?

“How has there not been updated flood mapping periodically?”

900 properties at risk

In October 2022, Kensington Banks escaped flooding when the adjacent Maribyrnong River burst its banks and flooded 600 properties upstream.

Many of those residents did not know of the flood risk until the water was on their property.

An independent review of the floods found Melbourne Water was using out-of-date modelling and didn’t factor in the impacts of climate change.

Under the new modelling, 900 properties in Kensington Banks have been designated as being at risk of flooding.

In a once in 100-year flood event, the average flood depth in the affected area would be half-a-metre.

Ninety per cent of properties would have a flood depth of less than one metre, but for some properties in Kensington Banks, the maximum flood depth is two metres.

Since a review of the 2022 floods, Melbourne Water must update its flood modelling every decade and review the data every five years.

The authority’s new flood modelling for its other catchments will be completed by 2026, with other areas likely to be identified as at risk of inundation. Managing director Nerina Di Lorenzo told 7.30 that there could be large-scale change.

“The technology at the time that Kensington Banks was developed was the late 90s,” Ms Di Lorenzo said.

“What we’re able to do today is so much more granular.

“Our challenge now is the challenge of climate change, and to face into that we’ve got to be ready to plan ahead and we’ve got to have the best data to do that.

“Anywhere on 25,000 kilometres of waterways, we might see some change.”

Uninsurable properties

The reviews will likely be cold comfort to home owners in the area.

Climate Valuation CEO Karl Mallon says as flood models around the country are updated, new flood zone areas will be announced.

“I think what we’re seeing in places like Kensington, we’re just going to see that over and over and over again,” Mr Mallon told 7.30.

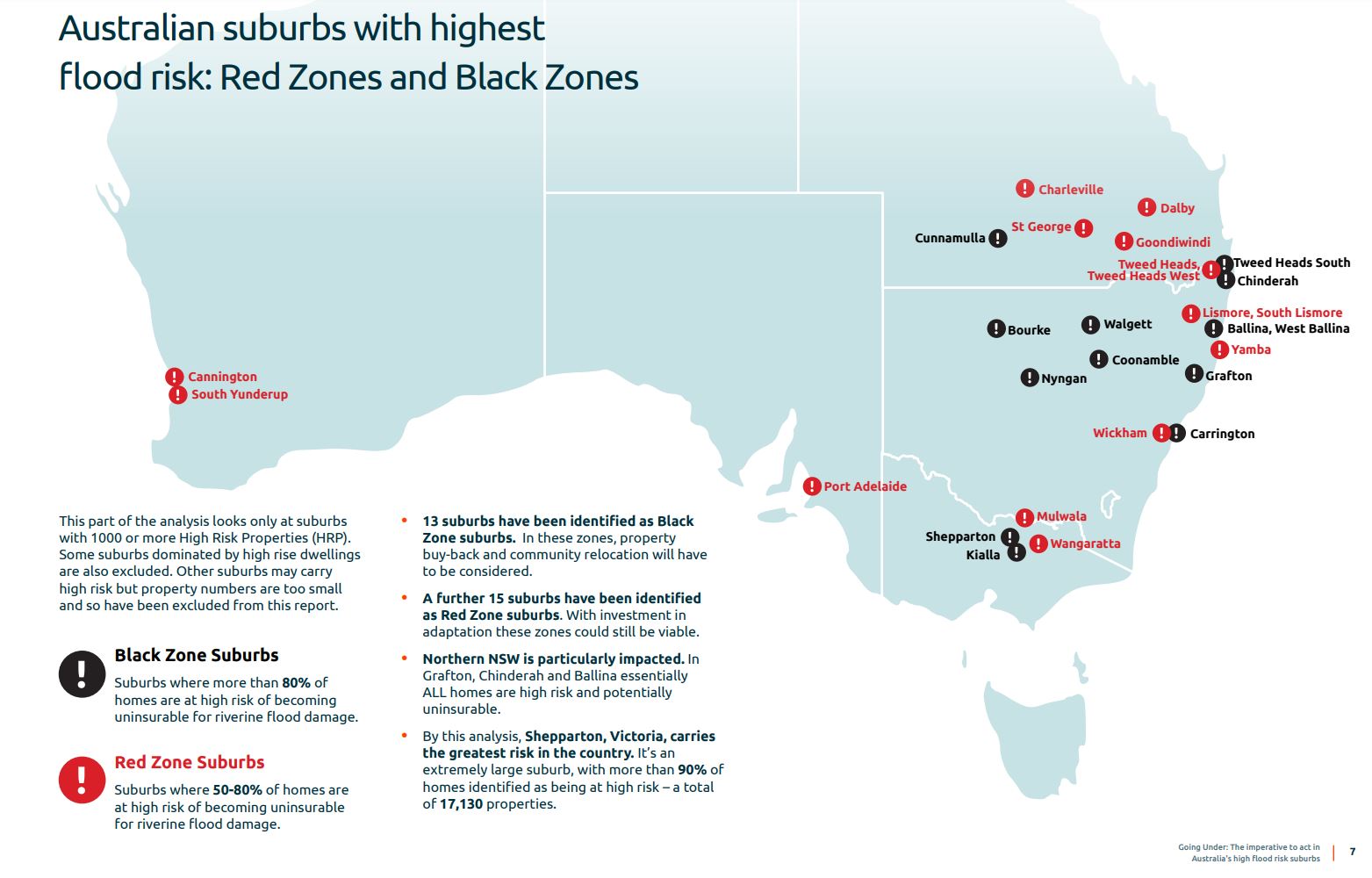

The analysis excluded smaller locations like Kensington Banks with fewer than 1,000 high-risk properties, or those dominated by high rise apartments.

The analysis focuses on homes identified as ‘high-risk properties’ by 2030 — where insurance may become unaffordable or withdrawn completely.

Climate Valuation defines high-risk properties using the word ‘uninsurable’ when the insurance premium is more than 1 per cent of the cost to replace the building.

“What that means is that insurance will either be unavailable, or it will be too expensive to afford when more than half of the suburb is in that position,” Mr Mallon said.

“That really is an alarm bell that something has to be done.

“We’re starting to see that process becoming widespread in Australia and around the world, where we’re seeing insurance withdrawn and we think there has to be urgent intervention.”

The report indicates that by 2030, over three million Australian homes are estimated to have exposure to some level of riverine flooding, and over half-a-million are expected to be considered high risk.

That means they carry a high risk of flood cover becoming prohibitively expensive or withdrawn.

In the Climate Valuation report, 13 suburbs have been identified as black zones. In these zones, property buyback and community relocation would have to be considered, according to the report.

A further 15 suburbs have been identified as red zones, where with investment in adaptation these zones could still be viable.

“Our red zone classification means that more than 50 per cent of the properties are at risk of becoming uninsurable — a community like Lismore would be in that categorisation,” Mr Mallon told 7.30.

“The black zone is even worse — that means that more than 80 per cent of the properties in that area are what we would be classified as high risk of becoming uninsurable due to flooding.”

Banks taking action

Real estate agents expect the new flood zoning could result in Kensington Banks property prices falling by 20 per cent, while insurance premiums are expected to rise.

Property owners in newly designated flood zones, who purchased their property in recent years, could also find their home is valued at less than the amount they owe the bank.

Mr Mallon said banks were factoring in climate change when writing new loans.

“What we are seeing is banks around the world start to say ‘we’re not going to issue mortgages on properties where either you can’t get insurance now or we as the bank don’t believe that, you’re going to be able to get affordable insurance for the life of the mortgage’,” Mr Mallon said.

“They’re looking at 30 years forward and they are including climate change into those calculations.

“Our view is that we’re going to see places where it’s going to be very hard to get a mortgage.”

Mr Hadgraft is hopeful mitigation could lower the flood risk for Kensington Banks and is calling for Melbourne Water’s modelling to be independently reviewed.

He is also among a number of Kensington Banks residents calling for the nearby Flemington Racecourse flood wall to be removed – a measure Melbourne Water has rejected.

An individual property assessment predicts his home would be inundated by about 30 centimetres of water.

Mr Mallon said there should be a nationally consistent approach to flood modelling that includes climate change impacts, made freely available to the public.

“We need a consistent approach to people in risk zones, there needs to be something which says that if you’re in this zone, you’re eligible for a buyback, if you’re in this zone, you’re eligible for an adaptation grant,” he said.

Victoria flags buybacks

There have already been calls for the Victorian government to commit to property buybacks for owners living in flood zones.

State water minister Harriet Shing did not rule that out and said Kensington Banks was developed based on the best information available to authorities at the time.

“I’d really like to see what the mitigation options look like and once we have a sense of the best advice on how to mitigate risk across our catchments,” Ms Shing told 7.30.

“Not just in one particular part of the Maribyrnong and Melbourne Water catchment but around the state.”

Mr Mallon says the reality is state, federal and local governments across Australia will need to face the consequences of past planning decisions and work with home owners in new flood zones.

“If you’ve allowed continued … or new development in a flood zone, there has to be some responsibility towards those people who may not have realised they are buying new houses in flood zones.”

Watch 7.30, Mondays to Thursdays 7:30pm on ABC iview and ABC TV

Posted , updated