This week’s interest-rate cut is a milestone for the European Central Bank.

Author of the article:

Bloomberg News

Mark Schroers and Alice Gledhill

Published Jun 03, 2024 • 6 minute read

You can save this article by registering for free here. Or sign-in if you have an account.

m56b6t0bahz7k7o99q4hxbb{_media_dl_1.pngBloomberg

Article content

(Bloomberg) — This week’s interest-rate cut is a milestone for the European Central Bank.

For the first time in two decades policymakers get to start a monetary-easing cycle without having their hand forced by a financial emergency. Instead, investors are signaling confidence about the euro area and keeping yields in check.

But despite the calm on the surface, the economy is starting to see the consequences of problems that have been decades in the making. Increasingly eclipsed by the dynamism of the US and the rise of China, the euro zone is languishing with anemic growth, weak productivity, poor demographics, and bloated public finances in key countries.

Advertisement 2

This advertisement has not loaded yet, but your article continues below.

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, Victoria Wells and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, Victoria Wells and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account.

Share your thoughts and join the conversation in the comments.

Enjoy additional articles per month.

Get email updates from your favourite authors.

Sign In or Create an Account

or

Article content

Benign markets and a recovering economy offer Brussels and national capitals rare breathing space to try to address those challenges. If politicians — navigating European elections this week — don’t take advantage to deliver growth-enhancing reforms and public-finance repair soon, the region risks sliding ever further into irrelevance.

“Without a major jolt, the European Union will become a much-diminished global power, leaving the US battling it out with China for economic supremacy,” said Jamie Rush, chief European economist for Bloomberg Economics.

The sense of a turning point for the euro region right now is palpable. The ECB rate cut comes as worst bout of inflation in the currency’s history seems largely over and a shallow recession just ended with an unexpected growth surge.

The spread between Italy’s bonds and German equivalents, a key measure of risk, narrowed earlier in 2024 to a two-year low. While yields have risen somewhat as investors assess just how much the ECB can cut given a more resilient than expected economy, there’s no sign of the fragmentation fears that stalked the market before the first hike in 2022.

Top Stories

Get the latest headlines, breaking news and columns.

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Top Stories will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

Advertisement 3

This advertisement has not loaded yet, but your article continues below.

Article content

“‘Europe’s a basket case’ — it’s all you ever used to hear” from investors outside the region, said Roger Hallam, global head of rates at Vanguard Asset Management. “You don’t hear that now.”

Supporting that view is a more cohesive policy backdrop at regional level, encompassing the European Union’s previously unthinkable pandemic-era recovery program — NextGenEU — that even involved the pooling of debt, and new crisis-fighting tools unveiled by the ECB to deliver stimulus and to keep bond markets in check.

Evidence of the region’s resilience emerged last year when investor panic brought down banks in the US and Switzerland. There were no such casualties in the euro zone, which will mark a decade of a unified supervision regime later this year.

And yet the region’s long-term problems look more ominous than ever.

“While Europe is doing better now, deep structural challenges — aging, climate change, and global fragmentation — await,” Alfred Kammer, a senior official at the International Monetary Fund, warned in May.

Weak productivity — and with it, poor potential growth — is one such problem. The EU as a whole has done consistently worse than the US on that since the current century dawned. Slower improvements in living standards and a “decline in global economic power” are the outcome, the European Centre for International Political Economy said in a study in May.

Advertisement 4

This advertisement has not loaded yet, but your article continues below.

Article content

The gap between the European and US economies since 2000 reached about 18% of potential GDP in 2023 — equivalent to more than €3 trillion ($3.3 trillion), according to Bloomberg Economics, which reckons the shortfall will reach almost 40% by 2050.

“It is on us as Europeans to do more,” German Finance Minister Christian Lindner told reporters in Italy last month at a meeting with peers that focused on the disparity between the US and Europe.

Another major problem is an aging population — adding to low potential growth and debt sustainability concerns, not least since pensions across the region are largely publicly funded out of current tax revenues.

“The birth rate is much worse than expected,” said Oliver Rakau, an economist at Oxford Economics. “This is not a problem in two, three or five years, but it is a big problem in the longer-run.”

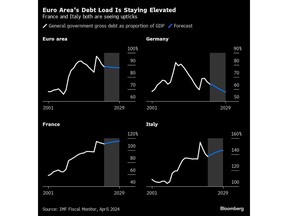

Most pressing is the deterioration of public finances in countries already struggling to impose fiscal restraint. Italy will have Europe’s biggest pile of borrowings in just three years, according to Scope Ratings.

IMF forecasts now show debt as a percentage of gross domestic product creeping up there and in France and Belgium — with deficits well above the 3% ceiling that the EU seeks to enforce.

Advertisement 5

This advertisement has not loaded yet, but your article continues below.

Article content

While bond markets show investors to be unperturbed, the region’s previous sovereign turmoil offers salutary lessons in how quickly sentiment can shift.

“The risks are rising,” said Moritz Kraemer, chief economist at LBBW and a former senior ratings analyst at S&P Global Ratings. “I think there’s not enough anxiety in the market.”

For all the effort that governments might make to bring debt deficits under control through spending cuts or tax increases, their best prospects to repair public finances in the long run will be through achieving better economic growth.

That’s one area where EU-level ideas are currently proliferating.

In mid-April former Italian Prime Minister Enrico Letta presented a report on the future of the bloc’s single market. Among other things, he urged consolidation for telecom operators and further integration of energy markets.

Former ECB President Mario Draghi will soon publish an eagerly-awaited report on the future of European competitiveness, which will attempt to stop the rot with a call for “radical change” that could include a lower regulatory burden and, in some cases, massive subsidies.

Advertisement 6

This advertisement has not loaded yet, but your article continues below.

Article content

“Without strategically designed and coordinated policy actions, it is logical that some of our industries will shut down capacity or relocate outside the EU,” he said in April.

Meanwhile French president Emmanuel Macron is pursuing an agenda of his own that includes pushing for greater capital market integration to emulate the success of the US in creating huge pools of finance.

“My concern is not just France, it is Europe in comparison with the US and China,” he told Bloomberg last month. “My top priority is to have a European policy saying we have to be much more innovative, we have to create a much more efficient capital market, we have to invest much more from a common budget as Europeans and from the private sector.”

There’s arguably greater momentum than usual to the EU’s drive for self improvement, even if the bloc has never been short of ideas that struggle to come to fruition.

“I’m hopeful that, with both the Letta report and upcoming Draghi report and the EU elections acting as a sort of catalyst, there’s an opportunity for policymakers to focus on what matters,” said Paul Hollingsworth, chief European economist at BNP Paribas.

Advertisement 7

This advertisement has not loaded yet, but your article continues below.

Article content

But Konstantin Veit, a portfolio manager at Pimco, notes that Europe’s record of delivery isn’t great. “Such reports contain a lot of the right things, but, if history is any guide, probably little will actually be implemented,” he said.

Big reports and initiatives used to be a more normal way for European integration to proceed, as evidenced by its 1980s push to create one of its signature successes, the single Market.

But more recent innovations, such as Draghi’s creation of a market-calming tool in 2012 and the recovery fund measure during the pandemic, were born out of turmoil.

“I would love to see a NextGeneration EU 2.0 or even a permanent one, in combination with the capital markets union,” said Michala Marcussen, group chief economist at Societe Generale. “I hope that we don’t have to go through another crisis to move on.”