Jerome Powell’s remarks in the coming week will be closely parsed by investors for any clues on just how long the Federal Reserve is willing to wait before cutting interest rates.

Author of the article:

Bloomberg News

Reade Pickert and Craig Stirling

Published Apr 27, 2024 • 6 minute read

You can save this article by registering for free here. Or sign-in if you have an account.

(Bloomberg) — Jerome Powell’s remarks in the coming week will be closely parsed by investors for any clues on just how long the Federal Reserve is willing to wait before cutting interest rates.

The last time the US central bank chair spoke, he signaled that policymakers were likely to keep borrowing costs high for longer than previously anticipated, pointing to the lack of further progress on bringing inflation down, and to enduring strength in the labor market.

Advertisement 2

This advertisement has not loaded yet, but your article continues below.

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, Victoria Wells and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, Victoria Wells and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account.

Share your thoughts and join the conversation in the comments.

Enjoy additional articles per month.

Get email updates from your favourite authors.

Sign In or Create an Account

or

Article content

Article content

The latest price data, which showed stubborn underlying inflation, in tandem with expectations for a robust employment report on Friday, aren’t likely to lead the Fed chief to change his tune.

Powell will address reporters after the Fed’s rate decision on Wednesday, when the central bank is widely expected to hold borrowing costs at a more than two decade high. Expectations for rate reductions have been pushed further into 2024, and investors are now betting on two cuts at most by year-end.

Capping the week will be the monthly jobs report, offering a fresh look at the state of the US labor market. Economists see non-farm payrolls growth moderating to a still-strong pace in April amid stable, low unemployment.

What Bloomberg Economics Says:

“We expect Powell to make a hawkish pivot. At the minimum, he’ll likely indicate the median FOMC participant now expects ‘less’ cuts this year. In a more hawkish direction, he could hint at a chance of no cuts — or even suggest a hike might be on the table, though not the current baseline.”

—Anna Wong, Stuart Paul, Eliza Winger & Estelle Ou, economists. For full analysis, click here

Top Stories

Get the latest headlines, breaking news and columns.

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Top Stories will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

Advertisement 3

This advertisement has not loaded yet, but your article continues below.

Article content

We’ll also get updates on a quarterly, closely watched measure of employment costs, as well as monthly figures on job openings and manufacturing.

For more, read Bloomberg Economics’ full Week Ahead for the US

Looking north, Canada’s gross domestic product data for February may show a slight boost to the economy, granting the Bank of Canada options as it weighs when to pivot to easier policy.

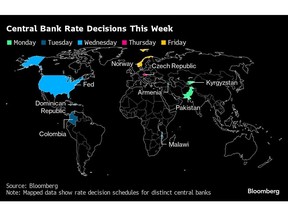

Elsewhere, euro-zone data may show inflation stopped slowing and the economy started to grow again, while Chinese surveys will point to the strength of expansion there. Central banks from Norway to Colombia will set rates, while the Paris-based OECD will release new global forecasts on Thursday.

Click here for what happened last week and below is our wrap of what’s coming up in the global economy.

Asia

China sheds light on prospects for building on first-quarter economic expansion with the release Tuesday of official purchasing manager index data. The report will indicate if manufacturing activity expanded for a second month in April.

There could be some seasonal softness resulting from fewer working days, but the overall thrust will probably point to a continuing recovery, according to Bloomberg Economics. Due the same day is the Caixin gauge, which has hovered over the 50 threshold that separates expansion from contraction for five months.

Advertisement 4

This advertisement has not loaded yet, but your article continues below.

Article content

Global commerce will be in the spotlight as Australia, South Korea, Thailand, Sri Lanka and Vietnam all release trade figures over the course of the week.

Japan gets a blast of data Tuesday that’s expected to show industrial output bounced back in March, with retail sales and the unemployment rate also set for release.

And South Korea’s consumer inflation data Thursday are forecast to show price growth slowing a touch while staying above the Bank of Korea’s target, giving the central bank added incentive to postpone any policy pivot.

For more, read Bloomberg Economics’ full Week Ahead for Asia

Europe, Middle East, Africa

In the euro zone, data may show that the slowdown in inflation stalled in April for the first time this year. Consumer prices probably rose 2.4% from a year earlier, matching the outcome for March, amid rising energy costs.

The underlying measure that strips out such volatile items may provide reassurance to officials that the direction of travel is still downward, though national numbers will probably reveal some divergence. Germany and Spain, due to release their data on Monday, may have experienced faster inflation.

Advertisement 5

This advertisement has not loaded yet, but your article continues below.

Article content

The euro-zone report comes on Tuesday along with the latest GDP numbers. Economists reckon the region probably returned to growth of a minimal 0.1% in the first quarter after the shallow recession it suffered in late 2023.

As with inflation, the numbers on Tuesday may mask uneven outcomes across the region. For a taste of that, investors are likely to watch closely for Ireland’s growth data on Monday, which has a history of volatility.

Overall, the reports might chime with European Central Bank President Christine Lagarde’s observation this month that the economy is weak and faces “bumps on the road” for the path of inflation.

Switzerland will release consumer price data on Thursday which may show inflation staying far below the 2% ceiling targeted by the central bank.

And the next day in Turkey, investors will be watching for progress in slowing consumer-price growth.

Most of the market sees the Turkish inflation rate continuing to quicken from March’s 68.5% to about 75% in the coming months, despite almost a year of aggressive rate hikes. Until price rises decelerate, bond investors are unlikely to rush back into the lira debt market, a key goal of Turkey’s government.

Advertisement 6

This advertisement has not loaded yet, but your article continues below.

Article content

A trio of monetary decisions take place across the wider region:

On Tuesday, Malawi officials may be persuaded to again raise the key rate to rein in inflation that’s likely to remain elevated due to crop damage from adverse weather conditions.

The Czech central bank is set to reveal its latest decision on Thursday, with policymakers expected to cut borrowing costs by 50 basis points.

The next day, Norges Bank may keep the deposit rate on hold after Norway’s economy developed better than expected, even as inflation slowed faster than projected. Investors will watch for clues on whether policymakers are growing more cautious about starting to cut borrowing costs in the autumn.

For more, read Bloomberg Economics’ full Week Ahead for EMEA

Latin America

Mexico’s first-quarter flash output data will likely show that the economy suffered a slight contraction from the three months through December. The consensus of analysts has growth slowing for a third year in 2023, to roughly 2.4% from 3.2% in 2023.

Brazil will post a number of reports, including the broadest measure of inflation, the central bank’s expectations survey, current account, industrial production and the national unemployment rate.

Advertisement 7

This advertisement has not loaded yet, but your article continues below.

Article content

Since last June, joblessness in Latin America’s biggest economy has been below 8%, which is viewed by many Brazil watchers as the economy’s non-accelerating inflation rate of unemployment.

Chile releases a slew of March indicators, including retail sales, unemployment, industrial production, manufacturing, copper output and GDP-proxy figures. Stronger-than-expected growth and a pick-up in inflation prompted the central bank to slow the pace of easing earlier this month.

In Peru, the April inflation report for the country’s mega-city capital of Lima may show prices finally back in the 1%-to-3% tolerance range, while still above the 2% target.

Colombia’s central bank is widely seen extending its easing cycle with a second-straight half-point cut that would lower the key rate to 11.75% amid a steady process of disinflation. BanRep will also post its quarterly inflation report, updating growth and inflation forecasts, as well as delivering a revised monetary policy outlook.

For more, read Bloomberg Economics’ full Week Ahead for Latin America

—With assistance from Robert Jameson, Laura Dhillon Kane, Vince Golle, Patrick Donahue, Brian Fowler, Monique Vanek, Paul Wallace and Ott Ummelas.