Bond investors who were torched yet again by robust economic data now want clear and conclusive proof that Federal Reserve interest-rate cuts are imminent before making any more big bullish wagers.

Author of the article:

Bloomberg News

Liz Capo McCormick and Michael Mackenzie

Published Apr 14, 2024 • 5 minute read

You can save this article by registering for free here. Or sign-in if you have an account.

9i3(ulb6r5l7lb{pnviuw3wq_media_dl_1.pngBloomberg

Article content

(Bloomberg) — Bond investors who were torched yet again by robust economic data now want clear and conclusive proof that Federal Reserve interest-rate cuts are imminent before making any more big bullish wagers.

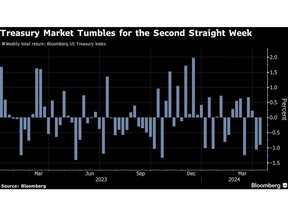

US yields surged to their highest levels of the year last week after traders were dealt the nasty surprise of a third straight month of sticky inflation. The market shock was accompanied by a wave of fresh short positions, with a growing camp of investors turning wary. Weak demand at the Treasury’s recent sales of long-term bonds provided even more evidence of bearish sentiment.

Advertisement 2

This advertisement has not loaded yet, but your article continues below.

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, Victoria Wells and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, Victoria Wells and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account.

Share your thoughts and join the conversation in the comments.

Enjoy additional articles per month.

Get email updates from your favourite authors.

Sign In or Create an Account

or

Article content

Article content

“The shorts have the Treasury market now,” said Andrew Brenner, head of international fixed income at NatAlliance Securities LLC. “We need to have numbers that back up the idea that rates need to be lower.”

Treasuries snapped their slide Friday and yields fell as tensions in the Middle East spurred a flight to safety. Iran’s unprecedented attack againt Israel on Saturday added to anxieties — and yet, while any further escalation may generate demand for US government debt as a haven, the current economic backdrop is more in line with an environment of higher rates for longer and pressure on bonds. Without convincing evidence of a change, few investors seem willing to swim against that tide.

After starting the year by pricing in as many as six rate cuts in 2024, or 1.5 percentage points of easing, traders are now doubtful there will even be a half point of reductions. Most Wall Street economists have dialed back forecasts as well, setting up a dour scenario for US yields including a possible repeat of maturities breaching 5% as they did last October.

Read more: Treasuries Haven Bid Gets Boost From Newly Added Big Bond Shorts

Top Stories

Get the latest headlines, breaking news and columns.

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Top Stories will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

Advertisement 3

This advertisement has not loaded yet, but your article continues below.

Article content

The recalibration in rate-cut expectations has been brutal for bonds. US Treasuries lost about 0.6% last week and are down some 2.6% for the year so far, according to a Bloomberg index. That’s a giveback of more than half of the 4.1% gain they posted in 2023.

Read more: First Fed Rate Cut Won’t Come Until December, Deutsche Bank Says

Even after Friday’s gains, the 10—year yield ended last week at 4.52%, with anticipated buying at the 4.5% level either not surfacing, or at the least not strong enough to fight the barrage of selling pressure.

“With US disinflation now stalling well above the Fed’s 2% target for three months straight, traders are acclimating to the prospect that the ‘last mile’ of disinflation is being tough to achieve,” said Thierry Wizman, global currencies and interest-rate strategist at Macquarie Group. A rise in 10-year yields to 4.75% “doesn’t look like much of a stretch” given where they are now, he added.

Federal Reserve Bank of Boston President Susan Collins said on Friday that it may take more time than previously thought to gain the confidence to begin easing policy, reiterating previous views. A day earlier, colleague NY Fed President John Williams said there was no clear need to adjust policy in the very near term.

Advertisement 4

This advertisement has not loaded yet, but your article continues below.

Article content

Read more: Fed’s Collins Penciled in Two Cuts This Year, No Urgency to Cut

This week, investors will get a read on consumer spending with the latest retail sales report, as well as new data on how the housing market is fairing with mortgage rates still high. Traders will also be parsing earnings from some of Wall Street’s biggest banks, with JPMorgan Chase & Co. shares falling Friday after its outlook for full-year net interest income missed expectations. Citigroup Inc.’s profits topped analysts’ estimates.

The minutes released on Wednesday from the Fed’s March gathering underscored officials’ reluctance to lower rates until they have more evidence inflation is firmly on a path to 2%. Consumer prices rose 3.8% in the 12 months ended in March, excluding food and energy.

Meanwhile, a growing chorus is questioning whether Fed policy is restrictive enough to crimp the labor market, despite the recent aggressive tightening cycle. Many traders now believe the so-called neutral rate, which neither stimulates nor restricts the economy, is much higher now than in the pre-pandemic era.

Advertisement 5

This advertisement has not loaded yet, but your article continues below.

Article content

What Bloomberg Intelligence Says…

“Rate markets have repriced into new ranges following the stronger-than-expected March US consumer price report and still-neutral Federal Reserve meeting minutes. The market is starting to hedge rate hikes as the next policy action, but the two-year yield may be discounting more symmetric outcomes.

— Ira F. Jersey, Will Hoffman, BI strategists

For the full note, click here.

Derivative traders see the funds rate hovering at just under 4% in about three years — well above Fed officials’ median forecast of 2.6% for their long-run rate.

“It’s possible” that the long-run rate is higher now than in the past, the Fed’s Collins said in an interview on Friday, adding that she’s working on this topic with her team to formulate a more clear view. “That’s something I’ll be focusing on because it’s an important question.”

There may be pressure on Fed Chair Jerome Powell and other policymakers to try to get at least one rate cut in a bit ahead of the US Presidential election in November because they don’t want to appear political, NatAlliance’s Brenner said. But the steady drip of strong economic data complicates things. “It’s clear Powell wants to ease and is looking for cover – but he can’t find it,” he said.

Advertisement 6

This advertisement has not loaded yet, but your article continues below.

Article content

While many expect upcoming Fed speakers to tilt to a more hawkish tone given the troubling inflation trend, some traders are reluctant to put their money behind what officials have to after all the seeming reversals. For others, there is a palpable sense of deja vu.

“So long as you see resilient data coming in, more questions will be asked about the Fed policy rate path,” said George Catrambone, head of fixed income at DWS Americas. “It feels a little bit of going back to 2023 — no recession, no landing and you just stay in cash.”

What to Watch

Economic data:

April 15: Empire manufacturing; retail sales; business inventories; NAHB housing market index

April 16: Building permits; housing starts; New York Fed services business activity; industrial production

April 17: MBA mortgage applications; Federal Reserve beige book; net TIC flows

April 18: Philadelphia Fed business outlook; initial jobless claims; leading index; existing home sales

April 19: Bloomberg US economic survey for April

Fed calendar:

April 15: Dallas Fed President Lorie Logan; San Francisco Fed President Mary Daly

April 16: Fed Vice Chair Philip Jefferson

April 17: Cleveland Fed President Loretta Mester; Fed Governor Michelle Bowman

April 18: Bowman; New York Fed President John Williams; Atlanta Fed President Raphael Bostic

April 19: Chicago Fed President Austan Goolsbee

Auction calendar:

April 15: 13-, 26-week bills

April 16: 42-day cash management bills; 52-week bills

April 17: 17-week bills; 20-year bonds

April 18: 4-, 8-week bills; five-year Tips

—With assistance from Edward Bolingbroke.

(Changes headline. adds information on Iran attack.)