A cadre of McKinsey & Co. consultants strode into a meeting with Houston’s most prominent local bank to dwell on the problem bedeviling thousands of regional banks: How to stay relevant.

Author of the article:

Bloomberg News

Todd Gillespie

Published Apr 09, 2024 • 4 minute read

You can save this article by registering for free here. Or sign-in if you have an account.

eprj3d9tmt4g0jonedurq0(m_media_dl_1.pngBloomberg

Article content

(Bloomberg) — A cadre of McKinsey & Co. consultants strode into a meeting with Houston’s most prominent local bank to dwell on the problem bedeviling thousands of regional banks: How to stay relevant.

“The thing that I laugh at, though, is they had a chart,” said Steve Stephens, the CEO of Amegy Bank, recalling the presentation to the board of its parent company in late 2022. McKinsey’s message was that banks such as Amegy could find a lucrative business niche, like the so-called specialty regional banks that it spotlighted in slides, he said.

Advertisement 2

This advertisement has not loaded yet, but your article continues below.

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, Victoria Wells and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, Victoria Wells and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account.

Share your thoughts and join the conversation in the comments.

Enjoy additional articles per month.

Get email updates from your favourite authors.

Sign In or Create an Account

or

Article content

Article content

“Well, that was First Republic, Silicon Valley Bank and Signature,” said Stephens, all of which collapsed last year. “It’s specialization that got them.”

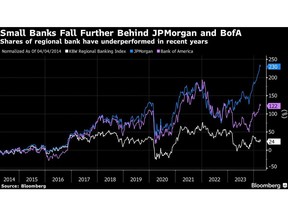

Across the US, thousands of small banks are trying to maintain their attractiveness as Wall Street lenders like Bank of America Corp. and JPMorgan Chase & Co. forge ahead in the tech-driven era of consumer finance. As many small banks continue relying on branches and local lending, their bigger rivals are building online ecosystems that seamlessly link deposit accounts, credit cards, wealth management and even dining and travel.

But for small banks, keeping up is proving tough at every turn. Mergers and acquisitions are slow. Chasing growth in niche business lines has proved perilous. And for firms that do manage to grow, there’s a ladder of ever-stiffening capital rules.

Amegy Bank is a microcosm of that swath of the American banking system. The lender had a front-row seat to the dangers afoot when its parent company, Zions Bancorp, got beaten up in the tumult last year, losing more than half its market value in two months.

Top Stories

Get the latest headlines, breaking news and columns.

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Top Stories will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

Advertisement 3

This advertisement has not loaded yet, but your article continues below.

Article content

Along with affiliates based in California and Utah, Amegy had been exploring growing its lending to the technology sector and was looking to SVB for inspiration. In the end, the group eschewed that route.

“We were fortunate enough that one of our executives had worked there, and he said it’s really not a lending strategy as much of a deposit strategy,” Stephens said in the interview at the firm’s offices in Houston. “That deposit base was actually a level of concentration they didn’t fully appreciate.”

It was a run on those deposits that led to SVB’s collapse early last year, as fleeing depositors forced it to sell assets at a loss after rising rates eroded their value. At that time, the industry’s giants grew as investors seeking safety sent deposits their way. The largest firms will start reporting first-quarter earnings later this week.

A representative for McKinsey declined to comment. That 2022 presentation was meant to provide an overview on the trends shaping the banking industry and the three failed banks were highlighted among about two dozen firms to showcase how investors were valuing them, according to another person who saw the deck and declined to be identified discussing private information.

Advertisement 4

This advertisement has not loaded yet, but your article continues below.

Article content

Amegy was created by a former heat pump salesman, Walter Johnson, in 1990 as another bout of banking turmoil crippled 600 Texas lenders who were exposed to losses on real estate and energy loans when oil prices fell. Johnson, now 88, started Amegy with $12 million, building it into the largest independent lender in Houston. He still shows up to work at Amegy Tower.

“He put together the first bank out of the ashes,” said Stephens, who was among the first hires. “He asks everyone he meets who they bank with, and he still brings in a new client once or twice a week.”

In 2005, Amegy’s owners sold it for $1.7 billion to Salt Lake City-based Zions, which owns seven banks across the US south and west. In 2023, deposits across the group totaled $75 billion, just under the amount of New York Community Bancorp Inc., the troubled real estate lender that struck a $1 billion rescue deal with investors led by former US Treasury Secretary Steven Mnuchin last month.

Read More: Winners of 2023 Bank Crisis Are Finding the New Spotlight Harsh

Last year’s turmoil triggered deposit outflows from Amegy, forcing it to sweeten the interest it paid customers to hold their money. Shares of its parent group have since recovered most of their losses.

Advertisement 5

This advertisement has not loaded yet, but your article continues below.

Article content

Many in the industry now expect a flurry of mergers and acquisitions as small banks club together or risk fading into irrelevance. Community banks, locally owned and operated, generally have less than $10 billion in assets. Most regionals, like Zions, have less than $100 billion — though a few super regionals have grown past $500 billion. JPMorgan and Bank of America have soared beyond $3 trillion.

Below the top tier, Stephens says consolidation is inevitable as thicker rule books strain small firms. Across his industry, he says he hears about the multitudes of “tired community bankers out there, because the regulations just eat you up.”

In the past, waves of consolidation have often followed turmoil.

“I don’t know what the trigger’s going to be,” he said. “They generally say when you have a mass of consolidation, it’s not like you’re out there proposing yourself — there’s an event when everybody’s running for cover. I don’t know if we’ll be an acquirer or an acquiree.”