US consumer-price data in the coming week, arriving on the heels of surprisingly strong jobs numbers, is projected to show a glacial slowdown in underlying inflation that explains the Federal Reserve’s cautious approach to lowering interest rates.

Author of the article:

Bloomberg News

Vince Golle

Published Apr 06, 2024 • 6 minute read

You can save this article by registering for free here. Or sign-in if you have an account.

(Bloomberg) — US consumer-price data in the coming week, arriving on the heels of surprisingly strong jobs numbers, is projected to show a glacial slowdown in underlying inflation that explains the Federal Reserve’s cautious approach to lowering interest rates.

The March core consumer price index, a measure of underlying inflation that excludes food and fuel, is seen rising 0.3% from a month earlier after a 0.4% advance in February. Wednesday’s report is expected to show a similar increase in the overall CPI.

Advertisement 2

This advertisement has not loaded yet, but your article continues below.

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, Victoria Wells and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, Victoria Wells and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account.

Share your thoughts and join the conversation in the comments.

Enjoy additional articles per month.

Get email updates from your favourite authors.

Sign In or Create an Account

or

Article content

Article content

The core price gauge is projected to have climbed 3.7% from a year ago, which would mark the smallest gain since April 2021. While the annual figure is well below the 6.6% peak reached in 2022, progress more recently has been uneven.

The closely watched inflation figures follow the latest monthly jobs report, which exceeded expectations for a fifth straight month. While Fed officials have pointed to moderating labor demand over the past year as a possible precursor to rate cuts, the 303,000 jump in March payrolls may raise questions over the extent of that cooling, and its implications for inflation.

Numerous Fed officials speaking over the past week were consistent in their messages that it’s appropriate to wait until there’s a clearer indication that inflation is slowing toward their target before taking the first step toward reducing borrowing costs.

What Bloomberg Economics Says:

“The focus now shifts toward the inflation trajectory, currently a more critical factor in the Fed’s reaction function. We expect the March CPI report to show a modest slowdown in the monthly pace of core inflation to 0.3% — which is still consistent with the Fed’s annual core PCE inflation target of 2.0%. Even if annual headline inflation flutters around 3.0% through year-end, persistent disinflation in the core should allow the Fed to cut rates this summer.”

Top Stories

Get the latest headlines, breaking news and columns.

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Top Stories will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

Advertisement 3

This advertisement has not loaded yet, but your article continues below.

Article content

— Anna Wong, Stuart Paul, Eliza Winger and Estelle Ou, economists. For full analysis, click here

US central bankers meet next on April 30-May 1 and are widely expected to hold rates steady. Minutes of their March gathering are due Wednesday, and traders will also monitor remarks from New York Fed President John Williams at an event on Thursday.

Read more: Blowout Jobs Data Raise Chance of Delayed, Fewer Fed Rate Cuts

A report Thursday on prices paid to US producers is forecast to show a more moderate monthly advance. Still, recent increases in the prices of crude oil, copper and some other commodities suggest less goods disinflation in the coming months.

For more, read Bloomberg Economics’ full Week Ahead for the US

Turning north, the Bank of Canada is widely expected to maintain its key policy rate at 5% on Wednesday, while revising economic projections to reflect stronger-than-expected growth at the start of this year and the long-term impacts of the Trudeau government’s cap on temporary residents.

Elsewhere, central banks from New Zealand to the euro area to Peru are also set to hold, while economists are split between a cut and a pause in Israel. Meanwhile, former Fed Chair Ben Bernanke is scheduled to deliver a review of Bank of England forecasting errors on Friday.

Advertisement 4

This advertisement has not loaded yet, but your article continues below.

Article content

Click here for what happened last week and below is our wrap of what’s coming up in the global economy.

Asia

A raft of central banks in Asia hold meetings in the coming week, with authorities in the Philippines, New Zealand, Thailand and South Korea all expected to hold policy steady.

The focus will fall on any hints indicating when they might pivot to easing cycles, with RBNZ Governor Adrian Orr expected to give an update Wednesday on the timeline for normalized rates as New Zealand’s economy continues to wobble.

In data, China’s consumer inflation is projected to slow to 0.4% in March, while the decline in producer prices may deepen a tad to 2.8%, backing the case for more stimulus. Exports are expected to drop for a second month.

India gets inflation figures for March and industrial output for February.

In Japan, cash earnings data may show real wages fell for a 23rd month in February, a trend that’s expected to end when wage hikes for the new fiscal year — the biggest in more than three decades — kick in.

For more, read Bloomberg Economics’ full Week Ahead for Asia

Europe, Middle East, Africa

Advertisement 5

This advertisement has not loaded yet, but your article continues below.

Article content

The European Central Bank is set to hold rates steady on Thursday in what’s universally expected to be the final such pause before it embarks on monetary easing in June. President Christine Lagarde’s words will be scoured for clues on what might happen after that, with some officials already pushing for back-to-back moves.

After last week’s weaker-than-anticipated inflation reading, policymakers won’t get much additional data ahead of the meeting, though the quarterly bank-lending survey on Tuesday may provide some insight.

European finance chiefs are scheduled to gather for their regular meeting in Luxembourg at the end of the week. They’ll discuss exchange-rate and inflation developments and the region’s competitiveness.

Turning east, Hungary is scheduled to publish minutes of its latest policy meeting, at which it lowered its benchmark by 75 basis points and said it would continue to dial back easing. Serbia is set to keep rates unchanged.

Russia gets inflation data on Wednesday, the same day that Bank of Russia Governor Elvira Nabiullina may present an annual report in the State Duma.

Advertisement 6

This advertisement has not loaded yet, but your article continues below.

Article content

In Britain, GDP figures on Friday are likely to confirm a second month of growth in February, putting the economy on track for a mild recovery after the shallow recession in 2023. The BOE that day will release a report from Bernanke, setting out recommendations for how officials can improve forecasting and communication after criticism they were slow to recognize the inflation crisis that started after the pandemic.

Israel’s rate decision on Monday is likely to be a close call between a hold and a 25 basis point cut. A decrease would boost the economy as the six-month war in Gaza continues to weigh on consumption and sectors from tourism to construction. But it could also add to pressure on the shekel, which has weakened since early March.

Uganda is likely to be more certain, with analysts predicting its monetary policy committee will leave the key rate unchanged after increasing it by 50 basis points to 10% at an unscheduled meeting last month. That’s as inflation has started to ease again and the currency is strengthening against the dollar.

For more, read Bloomberg Economics’ full Week Ahead for EMEA

Advertisement 7

This advertisement has not loaded yet, but your article continues below.

Article content

Latin America

Getting the inflation genie back in the bottle is giving central bankers around world fits, as Chile’s Rosanna Costa, Mexico’s Victoria Rodriguez and Brazil’s Roberto Campos Neto can attest.

Data in Chile will likely show consumer prices eased back near January’s 3.8% reading after jumping in February. The central bank has marked up its 2024 forecast to 3.8% from 2.9%.

In Mexico, where the disinflation process has proven bumpy and protracted, the early consensus is for both the full-month and bi-weekly readings to have re-accelerated.

Brazil, which actually got inflation below target as far back as last June before a 203 basis-point third-quarter surge, is likely to see consumer prices print lower for a sixth straight month, firmly within the central bank’s tolerance range but still well above target.

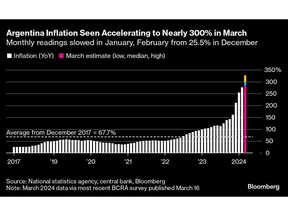

Last up is Argentina, where March monthly data out may post a single-digit rise, according to a member of President Javier Milei’s advisory council. Analysts surveyed by the central bank see it slightly over 14%, hot enough to send the year-on-year print up within a cat’s whisker of 300%.

Peru’s central bank on Thursday may go for a second straight rate pause at 6.25% after March inflation figures exceeded all economist estimates.

For more, read Bloomberg Economics’ full Week Ahead for Latin America

—With assistance from Robert Jameson, Brian Fowler, Laura Dhillon Kane, Reed Landberg, Paul Wallace, Monique Vanek, Tony Halpin and Alexander Weber.