The likelihood that central banks are about to embark upon the most synchronized reduction of interest rates since 2008 looks set to support the dollar in its nascent rebound.

(Bloomberg) — The likelihood that central banks are about to embark upon the most synchronized reduction of interest rates since 2008 looks set to support the dollar in its nascent rebound.

Wall Street came into the year betting that virtually every Group-of-10 currency would gain against the dollar on expectations that the Federal Reserve would unleash a series of aggressive interest-rate cuts. Instead, a gauge of the greenback has jumped more than 2% this quarter and the US currency has beaten most of its major peers.

Advertisement 2

This advertisement has not loaded yet, but your article continues below.

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, Victoria Wells and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, Victoria Wells and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account.

Share your thoughts and join the conversation in the comments.

Enjoy additional articles per month.

Get email updates from your favourite authors.

Sign In or Create an Account

or

Article content

Article content

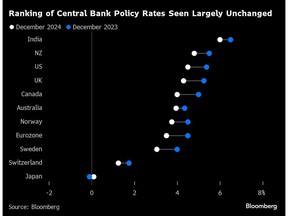

The dollar’s performance reflects both a recalibration of wagers on the extent of Fed cuts, but also a realization that the US will not be moving in isolation. Among the world’s 11 major central banks including the Fed, 10 are expected to cut rates in the second half of this year as global growth weakens, marking the most synchronized policy loosening cycle in 16 years, according to a Bloomberg analysis of economist forecasts and data from the Bank for International Settlements.

One of the few exceptions is the Bank of Japan, which just scrapped the world’s last negative interest rate and ended the most aggressive monetary stimulus program in modern history. That said, the well-telegraphed move also came with the caveat that the financial conditions will stay accommodative for now.

The dollar gained more than 3% on average in each quarter when 80% or more of those central banks eased policy in tandem, the analysis shows. The greenback is poised to retain such an advantage this time, as the Fed policy rate is forecast to remain the highest among major developed economies behind New Zealand’s at the end of this year.

Top Stories

Get the latest headlines, breaking news and columns.

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Top Stories will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

Advertisement 3

This advertisement has not loaded yet, but your article continues below.

Article content

“Unmitigated, aggressive short dollar bets risk being gloriously wrong,” said Vishnu Varathan, head of economics and strategy at Mizuho Bank Ltd. “It is unbelievably one dimensional to talk about the Fed’s pivot being a sure-fire short dollar bet. It is likely to be a mercurial beast, not a sanguine one that’s going to roll over and say ‘time’s up.’”

The seemingly contrarian prospect of a resurgent greenback may become more realistic as the world’s No. 1 economy continues to look resilient enough to avoid a recession, forcing markets to scale back expectations for aggressive policy easing. The dollar’s tailwinds also include its yield premium and a still robust US stock market that keeps attracting capital inflows.

‘Coming in Last’

Eight of the world’s 11 major central banks, including those of Europe and Canada, are expected to start easing policy from the second quarter along with the US, Bloomberg-compiled data show. The figure rises to 10 from the third quarter.

“Historically it was the US and the Fed that would be leading this macro narrative, and now the US and the Fed are coming in last” on easing, said Frances Donald, global chief economist at Manulife Investment Management, at an industry conference last month. “It’s very difficult for me to be bearish on the dollar because we just see the Fed and the US having a level of economic resiliency and exceptionalism that far outpaces” peers, she said.

Advertisement 4

This advertisement has not loaded yet, but your article continues below.

Article content

A strong US jobs market and sticky core inflation have prompted swaps traders to drastically push back bets on the timing and speed of Fed rate cuts. Powell suggested earlier this month that the Fed is getting close to the confidence needed to start easing, while his counterpart Christine Lagarde indicated the European Central Bank may be in a position to lower rates in June.

“When as we believe attention shifts to the policy differentials, currency markets can catch up,” said Alex Everett, investment manager of rates management at abrdn plc. “The greenback stands to perform here in the near term, fueled by continued economic strength and the remarkably benign glide path of inflation” lower.

Short Bets

Still, dollar bears remain the market’s dominant voice.

Since 2017, asset managers have clung to wagers that the dollar will fall, heightening the risk of a brutal trend reversal should those bets go awry. Wall Street strategists are also expecting virtually every Group-of-10 currency to gain against the dollar by the end of this year, with the euro strengthening to around 1.10 and the yen at 139.

Advertisement 5

This advertisement has not loaded yet, but your article continues below.

Article content

The dollar fell nearly 3% last year after consumer prices finally began easing after the Fed hiked rates aggressively. In addition, concerns about recession risks, the end of Japan’s negative rate regime, as well as rising Bitcoin and commodity prices may have also weighed on the greenback.

Bank of America is forecasting dollar strength to ebb in March and Goldman Sachs Group Inc. anticipates a weaker greenback in the long term. Citigroup Inc. favors selling the dollar.

Others say caution is warranted given the latest slew of data suggests the US economy is still healthy, while core inflation remains sticky. Demand for safe-haven assets may persist this year, given the ongoing wars in Ukraine and Gaza, slowing growth from Europe to China, and a slew of elections that will determine the leadership of over 40% of the world’s population.

“Dollar strength all the way through the second half is now our call,” said George Boubouras, head of research at hedge fund K2 Asset Management Ltd. “The US exceptionalism story is hard to ignore — we’re long dollars across our portfolios because this isn’t something you want to fight right now.”