Asian stocks are poised for a mixed start into a week that includes policy decisions from the Bank of Japan and Federal Reserve that will likely set the near-term direction for global markets.

Author of the article:

Bloomberg News

Matthew Burgess

Published Mar 17, 2024 • 4 minute read

kkh0d72er5jak34lj0n5tj7k_media_dl_1.pngBloomberg

Article content

(Bloomberg) — Asian stocks are poised for a mixed start into a week that includes policy decisions from the Bank of Japan and Federal Reserve that will likely set the near-term direction for global markets.

Australian equity futures point to a slight loss early Monday while Japanese and Hong Kong contracts showed small gains. The S&P 500 Index fell 0.7% on Friday, a move exacerbated by the expiry of derivative contracts tied to stocks, index options and futures.

Advertisement 2

This advertisement has not loaded yet, but your article continues below.

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, Victoria Wells and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, Victoria Wells and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account.

Share your thoughts and join the conversation in the comments.

Enjoy additional articles per month.

Get email updates from your favourite authors.

Sign In or Create an Account

or

Article content

Article content

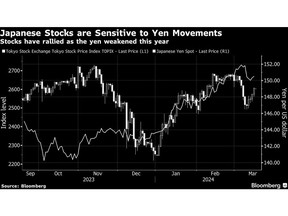

Japanese shares will be in early focus following reports that the BOJ may lift its key interest rate to 0%-0.1% on Tuesday, its first hike in 17 years. Speculation on the central bank exiting its negative rate policy intensified on Friday after Japan’s largest union group announced the strongest wage deals in more than three decades.

While swaps traders have priced about 28 basis points worth of rate hikes this year, they see the chance of a March hike at about 54%, according to data compiled by Bloomberg. The yen was little changed against the dollar in early Asian trading.

“We expect the BOJ to point out that although there is still a high degree of uncertainty about the future, it is now in a situation where it can see the achievement of the price target and it could likely abolish negative rates and yield-curve-control policies,” Societe Generale economists including Jin Kenzaki wrote in a note to clients. “However, at the same meeting, we also expect the bank to pledge to maintain interest rates at zero and 6 trillion yen per month in Japanese government bond purchases.”

Top Stories

Get the latest headlines, breaking news and columns.

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Top Stories will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

Advertisement 3

This advertisement has not loaded yet, but your article continues below.

Article content

Read More: Japan’s $4 Trillion to Stay Offshore After BOJ Hike: MLIV Pulse

Elsewhere in Asia, China’s economic activity due Monday was likely mixed at the start of the year with property remaining a major drag, raising doubts about the nation’s ability to gain momentum and hit an ambitious growth target of around 5%. The data, however, is unlikely to push the yuan out of its recent tight range, torn between China’s central bank and the upcoming Fed policy meeting, according to Commonwealth Bank of Australia.

“A potentially hawkish FOMC meeting can place upward pressure on dollar-offshore yuan” this week, CBA strategists led by Joseph Capurso wrote in a note to clients. But that “will likely be capped by the People’s Bank of China’s continued onshore yuan support at the daily fix.”

The Fed’s policy meeting Wednesday may dictate the direction of global stocks for the next quarter. Prior to the blackout period, Chairman Jerome Powell indicated the central bank was close to having the confidence to cut, while others debated how deep, or shallow, those declines will be.

Advertisement 4

This advertisement has not loaded yet, but your article continues below.

Article content

Bond traders, meanwhile, appear to have painfully surrendered to a higher-for-longer reality. Yields on policy sensitive two-year Treasuries have climbed 11 basis points this month to 4.73%, extending last month’s gain. Swaps traders are pricing about 71 basis points of rate cuts by year-end, down from 134 basis points at the start of the year, according to data compiled by Bloomberg.

“The Fed may have less confidence on inflation than before, but it still has confidence in the disinflation trend,” and may keep its median forecast of three cuts this year, Bank of America economists including Michael Gapen wrote in a note to clients. “This may be fanciful thinking on our part, but there are several inflation reports and plenty of time between now and June to change course if needed.”

Read More: Traders Look to Consumer Stocks for Clues on Where Fed Is Headed

Elsewhere this week, the Reserve Bank of Australia is set to extend its rate pause while Bank Indonesia and the Bank of England also deliver policy decisions. Eurozone inflation data is due as well as Reddit Inc.’s initial public offering.

Advertisement 5

This advertisement has not loaded yet, but your article continues below.

Article content

Key events this week:

China industrial production, retail sales, fixed assets, Monday

Eurozone CPI, Monday

Australia rate decision, Tuesday

Japan rate decision, Tuesday

Canada inflation, Tuesday

China loan prime rates, Wednesday

Indonesia rate decision, Wednesday

UK CPI, Wednesday

US rate decision, Wednesday

Brazil rate decision, Wednesday

ECB President Christine Lagarde speaks, Wednesday

New Zealand GDP, Thursday

Taiwan rate decision, Thursday

Switzerland rate decision, Thursday

Norway rate decision, Thursday

UK rate decision, Thursday

Mexico rate decision, Thursday

European Union summit in Brussels, Thursday

Japan CPI, Friday

Some of the main moves in markets:

Stocks

Hang Seng futures rose 0.2% as of 7:09 a.m. Tokyo time

S&P/ASX 200 futures fell 0.2%

Nikkei 225 futures rose 0.2%

Currencies

The euro was little changed at $1.0891

The Japanese yen was little changed at 149.10 per dollar

The offshore yuan was little changed at 7.2040 per dollar

The Australian dollar was little changed at $0.6559

Bonds

Australia’s 10-year yield advanced 4 basis points to 4.17%

Cryptocurrencies

Bitcoin was little changed at $68,228.6

Ether was little changed at $3,633.29

This story was produced with the assistance of Bloomberg Automation.