The theatre of Budget day may have allowed Chancellor Jeremy Hunt to set the stage for an election, by announcing major tax and spending plans.

It is the finer details of his script that could have a significant impact on your finances, so here is what his plans mean for you.

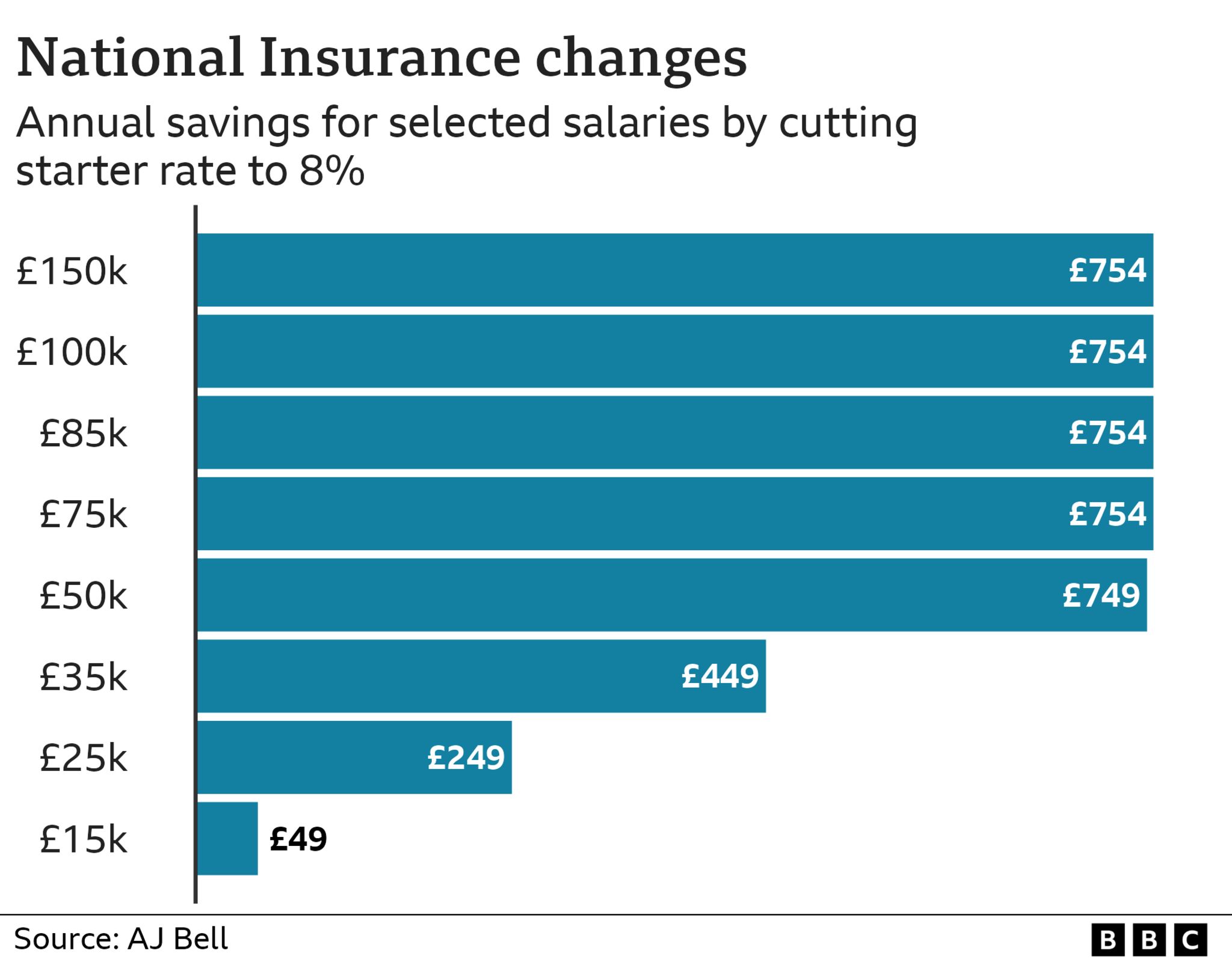

National Insurance to be cut

The chancellor’s big play to the audience was a cut in the rate of National Insurance (NI) paid by 27 million employees across the UK. A fixed percentage of the money you earn from your wages is deducted in NI.

January saw the first cut in Class 1 National Insurance for employees since at least 1975, according to available data, or possibly ever. Just three months later, there will be another one.

For employees paid between £12,571 to £50,270 a year, the current NI rate is 10% on earnings (down from 12% before January) and 2% on earnings above that. The chancellor said this would fall to 8% in April.

Someone earning £25,000 a year will save another £249 a year from the latest change. Higher earners will take home an additional £754 a year, according to calculations by investment companies.

For the self-employed, Class 4 NI contributions on all earnings between £12,570 and £50,270 were already due to be cut from a rate of 9% to 8% in April. Mr Hunt said that would now go down to 6%.

But more people will be paying tax

Existing government policy means income tax thresholds have been frozen since 2021, and will remain so until at least 2028. That means any kind of pay rise could drag you into a higher tax bracket, or will see a greater proportion of your income taxed than would otherwise be expected.

Normally, those thresholds are expected to rise in line with prices – so economists point out this has been the equivalent of £40bn tax rise.

The UK’s official forecaster, the Office for Budget Responsibility (OBR), has estimated as a result of the policy, 3.7 million more people will be paying income tax and 2.7 million will move into the higher bracket by 2028.

The effect of the combined 4p cut in NI and the threshold freezes from 2021 would mean that only those on £26,000 to £60,000 a year are better off in the next year, according to the Institute for Fiscal Studies.

Other taxes will be going up

Some councils have faced severe financial pressures, leading the majority to plan cuts to local services. Outside of Scotland (where it is frozen until 2025), they will raise council tax in April.

Councils in England have until 11 March to decide by how much. Those with social care duties can raise council tax by up to 4.99%, without triggering a referendum. Others can increase it by up to 2.99%.

Some can increase bills by more than 5%, with government permission, such as Birmingham where council tax will rise by 21% in two years.

Proposed increases vary from 3% to 16% in Wales, and between 4% and nearly 10% in domestic rates in Northern Ireland.

VAT – a tax added when you buy most goods and services – is unchanged.

Child benefit extended to more families

The point at which child benefit is withdrawn will now be at a higher level of earnings.

Instead of starting to lose child benefit once at least one parent earns over £50,000 a year, it will be £60,000. It will be taken away entirely from £80,000 a year, rather than £60,000.

The benefit is worth £24 a week for one child and £15.90 for each additional child. Those amounts are due to rise to £25.60 and £16.95 a week in April.

Overall, the government estimates 485,000 families will gain an average of £1,260 in child benefit in 2024-25 as a result, and 170,000 will avoid having to pay any back.

By April 2026, the plan is to move it to a system of household income, not that of individuals.

Cost-of-living support

Direct payments to people receiving benefits, pensioners and some with disabilities have been a lifeline for many in dealing with high prices and bills.

With the cost of domestic gas and electricity falling in April, no plans for any further cost-of-living payments were announced.

However, there was new funding for the Household Support Fund, which councils used to help those in need pay for essentials or have a warm place to go. This will be extended for another six months, having been due to end this month. Councils had called for two more years.

The £90 fee for debt relief orders, which helps some people write-off debts, will be abolished – although some had received grants for that. The repayment period for people on universal credit to pay back budgeting loans has risen from 12 to 24 months.

Fuel duty cut to be extended

Fuel duty is a tax motorists pay when buying fuels such as petrol and diesel.

It has been frozen since 2011, and this will continue. In fact, Mr Hunt extended a 5p-a-litre fuel duty cut, which was due to end this month, for a further year – keeping it at 53p a litre and saving the average car driver an estimated £50 next year.

Vaping and smoking to get more expensive

These so-called sin taxes will go up in time, and this time they will include a new duty on vaping.

Vaping products are already subject to value added tax (VAT). From October 2026, they will attract a separate levy. Duty on cigarettes will go up at the same time.

The cost of drinking will not rise, as the freeze on alcohol duty will be extended to February next year.

British Isa for savers

A new tax-free Individual Savings Account (Isa) will be available to savers. The money invested will be directed to British businesses.

Savers will be allowed to save £5,000 a year into the British Isa, on top of the existing Isa allowance of £20,000. No start date has been announced.

National Savings and Investments (NS&I) will offer British Savings Bonds for savers willing to lock their money away for three years in April. The interest rate is yet to be set.

Changes to property taxes

The government is already clamping down on holiday lets.

Now, in addition, the chancellor will scrap various tax breaks for holiday let owners. For example, there are allowances for furniture and the like which will go.

The higher rate of property capital gains tax will fall from 28% to 24% in April. That will benefit some people who sell a property which is not their home.

Non-dom tax status abolished

This is used by people who live in the UK, but whose principal home for tax purposes is elsewhere.

Non-domiciled people only pay UK tax on money earned in the UK. However, this status will be scrapped from April 2025 and replaced with a new system, potentially raising UK taxes for such people and raising revenue for the government.

Benefits, pensions and wages – what we already knew

The chancellor announced in the autumn that a range of benefits received by millions of people, such as universal credit, would rise by 6.7% in April, in line with the rate of rising prices (as of September).

Benefits are fully devolved in Northern Ireland, but changes will be similar to those for the rest of the UK.

The state pension, as previously announced, will go up by 8.5% in April, which means it will be worth:

- £221.20 a week for the full, new flat-rate state pension (for those who reached state pension age after April 2016)

- £169.50 a week for the full, old basic state pension (for those who reached state pension age before April 2016)

We also knew that the National Living Wage for over-23s – paid by employers – will rise from £10.42 an hour to £11.44 an hour in April, with increases for younger workers too.

How are you affected by the Budget? Do you have any questions? Get in touch by emailing [email protected].

Please include a contact number if you are willing to speak to a BBC journalist. You can also get in touch in the following ways:

If you are reading this page and can’t see the form you will need to visit the mobile version of the BBC website to submit your question or comment or you can email us at [email protected]. Please include your name, age and location with any submission.