Article content

(Bloomberg) — Ben Bernanke’s global savings glut is drying up. Long-term interest rates worldwide may be heading higher as a result.

Aging populations, an embattled Chinese economy and an increasingly fragmented global one are among the factors threatening to turn the surplus of savings the former Federal Reserve chair identified almost 20 years ago into a shortfall.

Advertisement 2

Article content

Article content

The result, according to some economists: A reversal of the decades-long trend toward lower interest rates as borrowers from Washington on down are forced to pay up for a dwindling supply of excess cash.

“We are entering an era of greater geopolitical rivalry and more transactional economic relations” that will depress the global supply of savings, former European Central Bank President and Italian Prime Minister Mario Draghi said in a recent speech. “The downward pressure on global real rates that has marked much of the era of globalization should be reversed.”

In 2005, Bernanke argued the world was awash with savings because China and other emerging markets were deliberately building up foreign-currency reserves as insurance against future financial crises. Oil exporters also had more money to invest, thanks to a surge in energy prices.

The result: Downward pressure on long-term interest rates around the world, including in the US. (Bernanke declined to comment for this article).

Read More: The Price of Money Is Going Up, and It’s Not Because of the Fed

Data compiled separately by Hanover Provident founder Robert Dugger and by Chicago Fed economists Robert Barsky and Matthew Easton suggest the glut crested some years ago. Its impact though was masked by the especially easy policies the Fed and other central banks hewed to coming out of the 2007-09 financial crisis. The pandemic subsequently triggered an even greater gusher of cash from the monetary and fiscal authorities as they fought to keep their economies afloat.

Top Stories

Article content

Advertisement 3

Article content

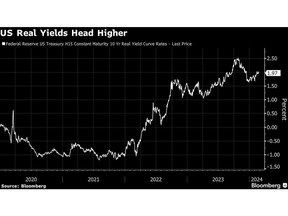

Now, with central banks scaling back interventions in global bond markets, the effects of the ebbing savings pool are starting to show through. Julian Brigden, co-founder of Macro Intelligence 2 Partners, sees rising real yields and a higher “term premium” on US Treasuries as a reflection of that phenomenon.

Brigden expects rates to go higher in coming years as aging societies spend down their savings, lifting what he calculates as fair value for the 10-year Treasury note to around 8% by about 2050 from roughly 3% now.

“We’ve deemed ourselves as structural bond bears for the next 30 years,” he said.

‘Politically Sustainable’

China’s role as a big supplier of savings to the rest of the world may also diminish as it’s pressured by the US on a variety of trade and technological fronts. The International Monetary Fund projects China’s savings will fall to 42.4% of its gross domestic product in 2028 from over 44% last year and 45.7% in 2022 as its current account surplus shrinks.

Business and economic models like China’s that are based on large trade surpluses “may no longer be politically sustainable,” Draghi told a meeting of the National Association of Business Economics on Feb. 15. “This change in international relations will affect the global supply of savings.”

Advertisement 4

Article content

IMF First Deputy Managing Director Gita Gopinath has warned of the risk of another Cold War, this time pitting the world’s two largest economies – the US and China – against each other.

“Threats to the free flow of capital and goods have intensified as geopolitical risks have grown,” she said in a speech in Colombia in December.

Draghi argued that will put a premium on coordination between fiscal and independent monetary policymakers that’s heretofore only been seen in economic emergencies like the pandemic.

In a scarce savings environment, governments will be seeking to fund such ambitious programs as the transition to net-zero carbon emissions, while central banks will be on guard against the danger that such stepped-up spending could trigger a burst of inflation.

The desirability of such enhanced coordination extends to the world’s biggest economy, where rising yields are already pushing the government’s interest costs to record levels.

“In a world of intensified competition for limited savings, success will require that the Fed and Congress pay attention to world savings availability and work together openly and continuously,” Dugger said.

Advertisement 5

Article content

Not all economists are convinced the world economy is entering a new era of higher interest rates. Yes, societies are aging. But people generally are also living longer. That prompts the elderly to spend down their savings more judiciously and the young to sock away even more for retirement, said former IMF chief economist Maurice Obstfeld.

Fed policymakers, for their part, have begun to entertain the possibility that the so-called neutral interest rate – the rate which neither spurs nor restricts the economy – may be higher than before the pandemic. But their focus is mainly domestic as they ponder the resilience of US economic activity in the face of sharply higher rates.

Dugger argues that they can’t ignore what’s going on worldwide.

“The Fed will not be able to push US rates below world levels without risking higher inflation — ‘higher for longer’ means what it says,” he said.

Article content