The pulse of US inflation likely continued to slow at the start of the year, helping to feed expectations that the Federal Reserve will find interest-rate cuts more palatable in the coming months.

Author of the article:

Bloomberg News

Vince Golle and Craig Stirling

Published Feb 10, 2024 • 6 minute read

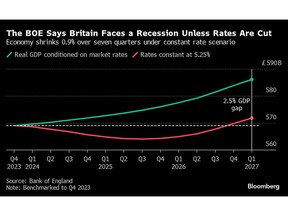

p3m47fcjxigfqqwa7[842[7a_media_dl_1.pngSource: Bank of England

Article content

(Bloomberg) — The pulse of US inflation likely continued to slow at the start of the year, helping to feed expectations that the Federal Reserve will find interest-rate cuts more palatable in the coming months.

The core consumer price index, a measure that excludes food and fuel for a better picture of underlying inflation, is seen increasing 3.7% in January from a year earlier.

Advertisement 2

This advertisement has not loaded yet, but your article continues below.

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, Victoria Wells and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, Victoria Wells and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account.

Share your thoughts and join the conversation in the comments.

Enjoy additional articles per month.

Get email updates from your favourite authors.

Article content

Article content

That would mark the smallest year-over-year advance since April 2021, and underscore the inroads Fed Chair Jerome Powell and his colleagues have made in beating back inflation. The overall CPI probably rose less than 3% for the first time in nearly two years, economists forecast Tuesday’s report to show.

While acknowledging that progress, policymakers have been cool to the idea that rates may be reduced as soon as next month.

Read More: Fed Officials Add to Chorus Tempering Hopes for Rate Cuts Soon

Their patience has roots in an economy that’s flashing green lights, the biggest of which is the labor market. Durable employment growth has kept consumers spending. A separate report on Thursday is projected to reveal another increase in retail sales, excluding motor vehicles and gasoline.

The cooling of inflation, along with expectations that borrowing costs will head lower this year, explains the recent improvement in consumer confidence. A University of Michigan survey scheduled for release on Friday is forecast to show an index of sentiment holding near the highest level since July 2021.

Top Stories

Get the latest headlines, breaking news and columns.

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Top Stories will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

Advertisement 3

This advertisement has not loaded yet, but your article continues below.

Article content

For more, read Bloomberg Economics’ full Week Ahead for the US

Investors will also monitor Fed officials speaking in the days following the CPI data, to gauge the timing of any future rate cut. Among those on the schedule are regional bank presidents Raphael Bostic of Atlanta and Mary Daly of San Francisco, who both vote on policy this year.

What Bloomberg Economics Says:

“In deciding when to start cutting rates, the Fed will have to reconcile the data they have in hand – which show inflation on a fast track to the 2% target — with risks that inflation could flare up again or the labor market could weaken more sharply. Data in the coming week will factor into that decision — but won’t provide a definitive answer.”

— Anna Wong, Stuart Paul, Eliza Winger and Estelle Ou, economists. For full analysis, click here

Turning north, Canadian home sales will reveal whether the market continues to heat up ahead of expected mid-year rate cuts. Housing starts and manufacturing data will also be released.

Among global highlights this week, Japanese gross domestic product, UK inflation and wages, and testimony by the euro-zone central bank chief will feature.

Advertisement 4

This advertisement has not loaded yet, but your article continues below.

Article content

Click here for what happened last week and below is our wrap of what’s coming up in the global economy.

Asia

Japan’s economy is expected to rebound from its dismal performance over the summer, providing another signal for the Bank of Japan as it prepares to end its negative rate policy.

Figures out Thursday are also set to confirm that Japan has slipped to the fourth-largest economy in the world, behind the US, China and Germany.

China’s markets will be closed for Lunar New Year celebrations, and no major releases are scheduled.

Reserve Bank of India Governor Shaktikanta Das, who kept a hawkish stance at Thursday’s rate meeting, may see some progress in his inflation fight at the start of the week with consumer prices expected to have grown at a slower pace in January. That probably won’t be slow enough to prompt talk of a pivot, however.

The Philippine central bank is seen holding rates steady on Thursday after prices continued to weaken there too.

Australian jobs figures earlier in the day are seen showing a return to growth after the losses in December.

Singapore will revise its gross domestic product figures ahead of trade data the following day.

Advertisement 5

This advertisement has not loaded yet, but your article continues below.

Article content

RBNZ Governor Adrian Orr sets out his latest position on policy and 2% inflation in a speech Friday morning, with Malaysian GDP numbers closing out the week.

For more, read Bloomberg Economics’ full Week Ahead for Asia

Europe, Middle East, Africa

UK data will take the limelight. On Tuesday, wage numbers may show the weakest pay pressures since 2022, cheering Bank of England officials who — like global peers — are pivoting toward rate cuts.

Policymakers will also scrutinize an anticipated blip higher in inflation on the headline gauge, and the core measure that strips out volatile elements such as energy, in data due Wednesday.

The next day, GDP will point to how BOE tightening is hitting growth. Economists reckon the UK stagnated in the fourth quarter, narrowly avoiding a recession for now.

Inflation data for January will also be released around the wider region this week:

Swiss consumer-price growth probably slowed to 1.6%, while Denmark will release equivalent numbers.

In Eastern Europe, inflation is anticipated to have weakened markedly in Poland and the Czech Republic, while edging higher in Romania.

In Ghana, the rate is likely to have eased from 23.2% a month earlier, while Nigeria’s reading may have accelerated from 28.9% amid currency weakness.

And in Israel, inflation is expected to have slowed to 2.7%.

Advertisement 6

This advertisement has not loaded yet, but your article continues below.

Article content

A series of fourth-quarter GDP numbers are also scheduled, with growth in Eastern European economies and Norway as well likely to have stayed subdued.

For more, read Bloomberg Economics’ full Week Ahead for EMEA

Euro-zone industrial production on Thursday is a highlight in the currency region, with a fourth monthly drop in December predicted by economists amid falling factory output in economies including Germany.

Policymaker appearances will draw attention. European Central Bank President Christine Lagarde testifies to lawmakers on Thursday, while multiple events featuring her colleagues are also scheduled.

In Norway, Governor Ida Wolden Bache will make her annual address to Norges Bank’s supervisory council.

A handful of rate decisions are on the calendar throughout the wider region:

In Romania on Tuesday, the central bank will probably keep its rate at 7% as investors watch for clues on potential cuts.

Zambian officials are poised to raise borrowing costs on Wednesday to support a battered currency and curb mounting price pressures.

The same day, Namibia’s policymakers will likely leave borrowing costs unchanged in line with South Africa’s pause last month.

And on Friday, the Bank of Russia may stay on hold after Governor Elvira Nabiullina indicated in December that the key rate will remain elevated for an extended period to tackle inflation running at almost double the 4% target.

Advertisement 7

This advertisement has not loaded yet, but your article continues below.

Article content

Latin America

The Carnival holiday makes for a quiet start to the week, but Argentina returns on Wednesday to post its January inflation report.

Consumer prices likely rose 21.9% last month, according to economists surveyed by the central bank, down from 25% in December. That forecast implies an annual rate of over 250%, up from 211% at year-end 2023.

Inflation has surged in the wake of President Javier Milei’s 54% peso devaluation and elimination of price controls on hundreds of everyday consumer products.

Colombia publishes a raft of data, underscoring the precipitous slowdown in what had been one of Latin America’s post-pandemic bright lights.

Industrial output, manufacturing and retail sales have all been negative since March, while fourth-quarter output probably shrank from the previous three months. Full-year GDP growth may only just top 1%, well off the 2021 and 2022 readings of 11% and 7.5%.

Brazil posts December GDP-proxy figures ahead of the quarterly and full-year report due March 1, while Peru publishes December economic activity data along with January unemployment for Lima, the capital and largest city.

Lastly, Chile’s central bank serves up the minutes of its January decision to deliver a 100 basis-point cut, to 7.25%. Economists surveyed by the central bank see that hitting 4.75% by year-end with inflation back at 3%.

For more, read Bloomberg Economics’ full Week Ahead for Latin America

—With assistance from Piotr Skolimowski, Robert Jameson, Monique Vanek, Brian Fowler, Abeer Abu Omar, Tony Halpin and Laura Dhillon Kane.