Asian bonds were poised to follow a slump in US Treasuries as strong economic data cut the likelihood of a quick Federal Reserve pivot to monetary easing. Stocks in the region were set for a mixed open.

Author of the article:

Bloomberg News

Jason Scott

Published Feb 05, 2024 • Last updated 1 minute ago • 6 minute read

86cs3kmeunba42aug93)c)08_media_dl_1.pngBloomberg

Article content

(Bloomberg) — Asian bonds were poised to follow a slump in US Treasuries as strong economic data cut the likelihood of a quick Federal Reserve pivot to monetary easing. Stocks in the region were set for a mixed open.

Australia’s 10-year benchmark yield climbed early Tuesday after Treasuries came under renewed pressure on speculation that optimism regarding disinflation may have gone too far. Shares in Sydney fell and Tokyo equities were poised to open lower, while battered China-related stocks could enjoy a rare reprieve after a prolonged selloff.

Advertisement 2

This advertisement has not loaded yet, but your article continues below.

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, Victoria Wells and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, Victoria Wells and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account.

Share your thoughts and join the conversation in the comments.

Enjoy additional articles per month.

Get email updates from your favourite authors.

Article content

Article content

On Wall Street, both bonds and stocks fell on Monday after data showed the Institute for Supply Management’s services gauge hit a four-month high while prices picked up. The news jolted trading when investors were already digesting cautious views from some Fed speakers including Jerome Powell.

The “one-two punch” prevented market players from achieving further upside, according to Jose Torres at Interactive Brokers. JPMorgan Chase & Co. strategist Marko Kolanovic said that “absent a material shock, we think this year’s easing will prove more moderate than markets have priced.”

US 10-year yields climbed 14 basis points to 4.16% and those on two-year notes approached 4.5%. Fed swaps almost wiped out the odds of a March rate move, and the chances of a May cut have also been reduced. The dollar hit its strongest since November. The S&P 500 fell from a record high — but came well off session lows as Nvidia Corp. led gains in chipmakers.

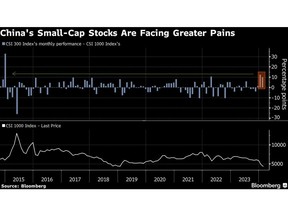

In Asia, focus will return to China, where concern over the torpid economy has spilled over into a deepening stock rout. That’s led authorities to tighten trading restrictions on domestic institutional investors as well as some offshore units. Meanwhile, the nation’s smallest stocks are flashing a warning about the potential downside for the world’s second-largest equity market if Beijing fails to follow through on a highly anticipated rescue campaign.

Top Stories

Get the latest headlines, breaking news and columns.

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Top Stories will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

Advertisement 3

This advertisement has not loaded yet, but your article continues below.

Article content

Annual wage negotiations in Japan have kicked off in earnest, as its central bank looks for evidence of a virtuous wage-price cycle that would allow it to exit from the world’s last negative rate regime.

Meanwhile, the Reserve Bank of Australia will release updated forecasts at its first policy meeting of the year on Tuesday, with economists unanimously expecting the cash rate will be kept at 4.35%. Authorities are expected to maintain a hawkish stance given inflation, while cooling, is still elevated.

In the US, traders also waded through remarks from Fed speakers, with Powell reiterating that policymakers will likely wait beyond March to cut rates in an interview conducted Thursday with CBS’s 60 Minutes that aired Sunday evening. Fed Bank of Minneapolis President Neel Kashkari said officials have time to gauge incoming data before easing while his Chicago counterpart Austan Goolsbee reiterated he’d like to see more of the favorable inflation data.

To Thierry Wizman at Macquarie, the shift in the market’s assessment of when the Fed will begin to cut rates seems valid.

Advertisement 4

This advertisement has not loaded yet, but your article continues below.

Article content

“We had always thought that June was the likelier month for a cut in view of the Fed’s prudence,” Wizman noted. “What does worry us, though, is whether the ongoing strength of the US job market in January means that the US consumer will stay strong, thereby undoing the disinflationary trend, and extending tight monetary policy more indefinitely.”

The ISM’s overall gauge of services increased to 53.4 last month. The index has remained above the 50 level that indicates expansion for a year. The latest reading exceeded all estimates in a Bloomberg survey of economists. The group’s metric of prices paid for materials jumped — showing that costs are rising at a faster pace.

Jeffrey Roach at LPL Financial says the big uptick in prices paid mostly reflected the increase in shipping costs. Investors should expect prices to revert if conditions in the Red Sea improve, he added.

The world’s major central banks mustn’t drop their guard in the fight against inflation as it’s too soon to say if sharp interest rate increases have contained underlying price pressures, the OECD said. Meantime, the latest Bloomberg Markets Live Pulse survey showed American shoppers won’t be deterred by mounting credit-card bills or the recent ripple of layoffs. More than half of 463 respondents said spending will stay strong or get even stronger in 2024.

Advertisement 5

This advertisement has not loaded yet, but your article continues below.

Article content

“The ongoing strength of the US economy relative to most of its G-10 peers is one of the key reasons why we have held a counter consensus bullish view on the USD since September 2023,” said Dominic Bunning at HSBC. “The strength of activity data will, in our view, make it hard for the Fed to have confidence that inflation is fully tamed. As such, we see rate pricing in the US being more prone to upside than downside for now.”

With the S&P 500 coming off its best stretch in nearly four decades, the road gets tougher for investors as the calendar flipped to February. It’s the third-worst month for the gauge in the past 30 years, behind September and August, according to data compiled by Bloomberg.

Corporate Highlights:

Boeing Co. found more mistakes with holes drilled in the fuselage of its 737 Max jet, a setback that could further slow deliveries on a critical program already restricted by regulators over quality lapses.

Caterpillar Inc., one of the world’s largest manufacturers of heavy machinery, batted away concerns of a global economic slowdown after reporting higher fourth-quarter sales in its energy and transportation business, which helped it to post profit that topped analysts’ expectations.

The US Attorney’s Office in Manhattan has launched an investigation into the accounting practices at Archer-Daniels-Midland Co., according to people with direct knowledge of the matter.

McDonald’s Corp.’s sales missed investor expectations in the fourth quarter as growth decelerated, hurt in part by the conflict in the Middle East.

Tyson Foods Inc. posted quarterly earnings that beat even the highest of analysts’ estimates.

Snap Inc. is reducing its workforce by roughly 10% worldwide, joining the chorus of technology companies that have announced fresh rounds of cuts in 2024.

Estée Lauder Cos. said it’s cutting as many as 3,000 positions as part of a restructuring plan to put one of the world’s largest beauty companies back on track.

Advertisement 6

This advertisement has not loaded yet, but your article continues below.

Article content

Key events this week:

Reserve Bank of Australia’s rate decision, Tuesday

Eurozone retail sales, Tuesday

Germany factory orders, Tuesday

UBS earnings, Tuesday

Bank of Canada Governor Tiff Macklem speaks, Tuesday

Fed’s Loretta Mester and Patrick Harker speak, Tuesday

Germany industrial production, Wednesday

Walt Disney earnings, Wednesday

Fed’s Adriana Kugler and Tom Barkin speak, Wednesday

China PPI, CPI, Thursday

US wholesale inventories, initial jobless claims, Thursday

Treasury Secretary Janet Yellen speaks at a Senate banking committee hearing on the Financial Stability Oversight Council annual report, Thursday

Pharma CEOs speak at a Senate panel on prescription drug prices, Thursday

ECB Chief Economist Philip Lane speaks, Thursday

ECB publishes economic bulletin, Thursday

US CPI revisions, Friday

Germany CPI, Friday

President Joe Biden hosts German Chancellor Olaf Scholz at the White House, Friday

Some of the main moves in markets:

Stocks

S&P 500 futures were little changed as of 8:20 a.m. Tokyo time

Hang Seng futures rose 0.5%

Nikkei 225 futures fell 0.1%

Australia’s S&P/ASX 200 fell 0.5%

Currencies

The Bloomberg Dollar Spot Index rose 0.4%

The euro was unchanged at $1.0743

The Japanese yen was little changed at 148.66 per dollar

The offshore yuan was little changed at 7.2198 per dollar

Cryptocurrencies

Bitcoin rose 0.3% to $42,462.32

Ether rose 0.2% to $2,291.9

Bonds

The yield on 10-year Treasuries advanced 14 basis points to 4.16%

Australia’s 10-year yield advanced four basis points to 4.13%

Commodities

West Texas Intermediate crude was little changed

Spot gold was little changed

This story was produced with the assistance of Bloomberg Automation.